Author: Denis Avetisyan

New research reveals a direct causal link between the language used in financial reports and a bank’s bottom line.

A rigorous analysis using Causal Forests, XGBoost, and SHAP values demonstrates that sentiment in financial reports causally affects profitability, with effects moderated by a bank’s asset composition and balance sheet strength.

While correlational studies abound, establishing causal links between qualitative information and firm performance remains challenging. This research, ‘Beyond the Numbers: Causal Effects of Financial Report Sentiment on Bank Profitability’, addresses this gap by demonstrating that sentiment expressed in financial reports directly impacts bank profitability, contingent on factors like asset composition and balance sheet strength. Utilizing a causal forest machine learning framework-including XGBoost and SHAP value analysis-the study reveals statistically significant causal associations beyond traditional metrics. Could a deeper understanding of these causal pathways reshape financial analysis and risk management strategies?

Decoding the Narrative: Sentiment as a Financial Signal

For decades, financial health assessments have predominantly centered on numerical data – ratios derived from balance sheets and income statements. This approach, while providing a structured framework, often neglects the crucial qualitative insights hidden within the textual components of financial reports. Company filings, investor communications, and even executive statements contain nuanced language that reflects management’s outlook, perceived risks, and strategic direction. These textual signals, frequently overlooked, offer a valuable complement to quantitative analysis, potentially revealing subtle shifts in a company’s underlying health before they are fully reflected in the numbers. Ignoring this rich source of information represents a significant gap in traditional financial modeling, as human perception and market reactions are heavily influenced by the narrative surrounding financial performance, not solely by the figures themselves.

The language used within financial reports isn’t merely descriptive; it actively shapes how investors and stakeholders perceive a company’s risk profile. A subtly negative tone, even amidst positive financial figures, can trigger heightened caution and ultimately diminish anticipated returns. This phenomenon, captured by the metric `Financial Report Sentiment`, suggests that emotional cues embedded in textual disclosures profoundly influence financial decision-making. Research indicates that negative sentiment correlates with increased investor skepticism, potentially leading to decreased stock valuation and, consequently, a reduction in a company’s `Net Profit`. This highlights the critical role of qualitative data in supplementing traditional quantitative analysis, as perceptions of risk, heavily influenced by emotional tone, are demonstrably linked to tangible financial outcomes.

Sentiment analysis, increasingly vital in financial forecasting, leverages computational linguistics to distill emotional tone from textual data-specifically, financial reports. Models like FinancialBERT, a sophisticated iteration of the BERT language model, are trained on vast corpora of financial text, enabling them to discern nuanced sentiment with remarkable accuracy. This goes beyond simple positive or negative labeling; the system identifies the degree of optimism or pessimism, quantifying subjective language that previously existed outside traditional financial metrics. Consequently, analysts can now systematically extract and measure previously untapped qualitative information, moving from intuition-based assessments to data-driven insights regarding a company’s perceived health and potential risk.

Moving beyond merely identifying associations between textual sentiment and financial performance demands analytical sophistication. While correlations can suggest a link – for example, positive language in reports coinciding with higher net profit – they fail to prove that one directly influences the other. Establishing causality requires tools capable of controlling for confounding variables, accounting for temporal dynamics, and potentially leveraging techniques like Granger causality tests or instrumental variable analysis. Researchers are increasingly focused on developing models that can not only detect sentiment but also assess its predictive power while rigorously isolating it from other contributing factors, ultimately allowing for a deeper understanding of how language shapes financial outcomes and informs investment strategies. This necessitates a move toward more complex statistical modeling and a critical evaluation of the underlying mechanisms driving the observed relationships.

Beyond Correlation: Discerning Causal Mechanisms

Traditional statistical methods often identify correlations between financial report sentiment and net profit, but these associations do not necessarily indicate a causal relationship. Causal inference techniques address this limitation by explicitly modeling the mechanisms through which sentiment might affect profitability. These methods move beyond simply observing a link to actively estimating the effect of sentiment on net profit, accounting for other factors that could simultaneously influence both variables. By employing techniques like potential outcomes and counterfactual reasoning, researchers aim to isolate the specific impact of financial report sentiment, providing a more reliable understanding of its true effect on a company’s bottom line and enabling more informed investment strategies.

Causal Forests are a machine learning approach extending the Random Forest algorithm to estimate causal effects. Unlike traditional regression models, Causal Forests explicitly model the treatment assignment mechanism, allowing for estimation of Average Treatment Effects (ATE) even when treatment is not randomly assigned. The method constructs a forest of regression trees, partitioning the data based on observed covariates to create subgroups where treatment assignment is more closely approximated as random. By averaging the treatment effects estimated within each leaf node, weighted by the proportion of observations in that node, Causal Forests provide an estimate of the overall treatment effect. This framework effectively addresses confounding by controlling for observed covariates and can handle complex interactions and non-linear relationships without requiring explicit specification of interaction terms or functional forms.

Propensity Score Matching (PSM) is integrated with Causal Forests to address selection bias and improve the accuracy of causal effect estimation. PSM creates statistically comparable groups by matching firms with similar characteristics-based on their propensity scores-but differing levels of financial report sentiment. This reduces confounding by observable variables. Subsequently, Causal Forests are applied to these matched samples, leveraging their ability to model complex interactions and estimate heterogeneous treatment effects. By combining PSM’s bias reduction with Causal Forests’ flexibility, researchers can obtain more reliable estimates of the causal impact of financial report sentiment on net profit, even in the presence of unobserved confounders and complex relationships.

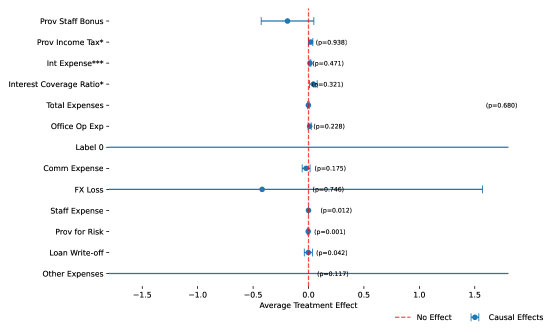

Analysis utilizing causal inference techniques demonstrates that the impact of financial report sentiment on net profit is not uniform across all firms. Research indicates heterogeneous effects, where balance sheet strength and asset composition significantly moderate the relationship. Specifically, firms with stronger balance sheets – characterized by higher liquidity ratios and lower debt-to-equity ratios – exhibit a more pronounced positive correlation between positive sentiment and profitability. Conversely, the influence of sentiment on firms with weaker balance sheets is diminished. Furthermore, asset composition plays a crucial role; firms with a greater proportion of liquid assets tend to benefit more from positive sentiment signals compared to those with primarily illiquid or fixed assets. These findings highlight that the effect of sentiment is contingent upon underlying firm characteristics and is not a universally applicable phenomenon.

Contextualizing Impact: Core Financial Indicators as Moderators

Financial report sentiment demonstrably impacts net profit in conjunction with core financial health indicators. Specifically, a firm’s ability to service its debt, as measured by the Interest Coverage Ratio, directly moderates the relationship between reported sentiment and profitability. Higher levels of interest expense, conversely, negatively correlate with the positive effects of favorable sentiment reporting. The Debt to Equity Ratio provides further context, indicating the degree of financial leverage and potential risk; firms with higher ratios may exhibit a diminished positive response to positive sentiment due to increased financial obligations. These indicators collectively demonstrate that sentiment’s influence on net profit is not isolated, but rather operates within the established framework of a firm’s financial structure and debt management capabilities.

A firm’s financial performance, as it relates to reported sentiment, is not solely determined by sentiment itself but is significantly modulated by underlying asset structure and lending practices. The composition of a company’s assets – the relative proportions of current versus non-current assets, tangible versus intangible assets, and the liquidity of those assets – influences its ability to absorb negative sentiment or capitalize on positive sentiment. Similarly, characteristics of the loan portfolio, including loan concentration, credit quality, and the presence of collateral, impact a firm’s vulnerability to economic downturns and its capacity to extend credit, which then interacts with the effects of sentiment on net profit. These factors introduce complexity, creating nuanced relationships between sentiment and profitability that necessitate a granular analytical approach.

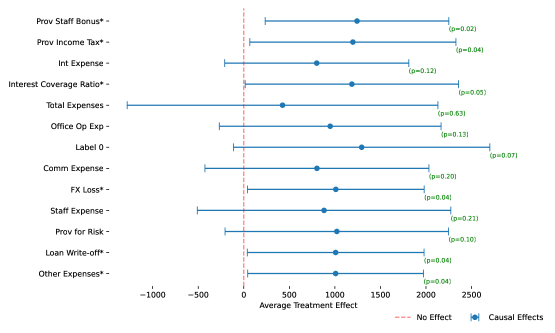

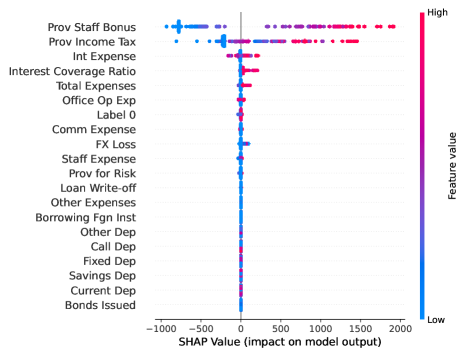

The application of SHAP (SHapley Additive exPlanations) values, in conjunction with machine learning models such as XGBoost, enables the decomposition of predictions to determine the contribution of each feature to the observed relationship between financial report sentiment and profitability. This methodology moves beyond simple correlation to establish feature importance by calculating the marginal contribution of each feature across all possible feature combinations. Specifically, SHAP values quantify the impact of a feature on the difference between the actual predicted outcome and the average predicted outcome, allowing for the identification of key financial indicators – like ‘Prov Staff Bonus’ or ‘Interest Expense’ – that most significantly drive the effect of sentiment on net profit. This granular level of analysis facilitates a deeper understanding of the underlying mechanisms connecting qualitative textual data with quantitative financial performance.

Analysis indicates that the impact of financial report sentiment on firm performance is not independent; rather, it is significantly modulated by underlying financial fundamentals. Statistical modeling using Average Treatment Effects (ATEs) revealed that ‘Prov Staff Bonus’ and ‘Interest Coverage Ratio’ exhibited statistically significant positive correlations with profitability (p < 0.05), suggesting that positive sentiment amplifies the effects of these factors. Conversely, ‘Int Expense’ demonstrated a statistically significant negative ATE (p < 0.01), indicating that positive sentiment is associated with a lessened negative impact from interest expense. These results demonstrate an interactive effect where sentiment acts as a catalyst or buffer in conjunction with specific financial variables.

Unlocking Future Value: From Prediction to Proactive Management

Recognizing that communication impacts investors differently is crucial for maximizing financial outcomes. Research demonstrates the existence of Heterogeneous Treatment Effects, meaning the same message doesn’t resonate equally with all investors. Firms are increasingly able to identify these varying sensitivities through data analysis, allowing them to personalize their communication strategies. By tailoring messaging to specific investor segments – perhaps emphasizing growth potential for one group and stability for another – companies can significantly amplify positive sentiment and, consequently, improve net profit. This shift from broad-stroke communication to targeted messaging represents a powerful evolution in investor relations, transforming sentiment analysis from a simple gauge of opinion into a tool for actively shaping it and driving financial success.

Sentiment analysis is rapidly evolving from simply describing public opinion to actively forecasting and guiding future outcomes. Historically, these techniques cataloged existing attitudes – gauging whether commentary surrounding a company was generally positive or negative. Current research demonstrates a capacity to predict how shifts in sentiment will likely impact key performance indicators, such as net profit, and even to prescribe targeted interventions – like tailored communication strategies – designed to optimize those outcomes. This transition signifies a powerful advancement; instead of merely reacting to market sentiment, organizations can now leverage data-driven insights to proactively shape investor perception and ultimately, enhance financial performance. The potential extends beyond individual firms, promising a more informed and resilient financial ecosystem capable of anticipating and mitigating risk with greater precision.

Financial modeling traditionally relies on quantitative data, but increasingly, incorporating sentiment analysis offers a more nuanced understanding of risk and potential returns. Studies demonstrate that investor sentiment, gleaned from sources like news articles, social media, and earnings call transcripts, correlates significantly with market fluctuations and individual stock performance. By integrating these sentiment indicators into existing models – alongside traditional financial metrics – analysts can refine risk assessments, potentially identifying undervalued assets or anticipating market corrections with greater accuracy. This allows for more informed investment decisions, moving beyond purely reactive strategies to a proactive approach that anticipates shifts in investor behavior and leverages emotional responses to maximize portfolio performance. The inclusion of sentiment data is not simply about predicting what will happen, but understanding why, thereby enhancing the predictive power and robustness of financial forecasts.

The integration of sentiment analysis into financial strategy signals a shift from reactive assessment to proactive management, potentially unlocking substantial value across multiple levels. By anticipating investor responses and tailoring communication, firms can not only mitigate risks but also actively cultivate positive perceptions that translate to increased net profit. This extends beyond individual gains; a widespread adoption of proactive sentiment-driven strategies promises a more stable and efficient financial ecosystem. Enhanced transparency and informed decision-making, facilitated by predictive analytics, can reduce market volatility and foster greater trust between companies and investors, ultimately driving sustainable growth and innovation throughout the financial landscape.

The pursuit of clarity in financial reporting, as demonstrated by this research, echoes a timeless principle. One might recall the words of Epicurus: “It is not the pursuit of pleasure itself that is evil, but the errors in our reasoning which lead us to pursue it.” Similarly, this study reveals that sentiment-a potentially fleeting emotional response-can have a causal impact on profitability, but only when understood through rigorous analysis. The application of Causal Forests, XGBoost, and SHAP values serves not merely to quantify this effect, but to dispel erroneous interpretations and reveal the underlying mechanisms at play, aligning with Epicurus’ emphasis on reasoned judgment. A well-constructed analysis, like a beautifully designed interface, becomes almost invisible-its power lies in its ability to reveal truth with elegance and precision.

The Road Ahead

The assertion of a causal link between the subtle language of financial reports and concrete profitability feels, at first glance, almost… elegant. Too many analyses settle for correlation, mistaking shadow for substance. This work, however, suggests that careful parsing of textual nuance does matter, though the effect is predictably contingent. The heterogeneity revealed – that asset composition and balance sheet strength mediate this relationship – is not surprising, but it does serve as a useful rebuke to overly simplistic models. The architecture of the analysis, relying on Causal Forests and bolstered by XGBoost and SHAP values, functions largely as it should-invisible until one attempts to force a less-refined method into service.

Yet, the inherent limitations of even the most sophisticated techniques remain. The study necessarily focuses on publicly available reports; the internal communications, the whispered caveats, the strategic omissions-these remain largely opaque. A truly comprehensive understanding would demand access to these hidden layers, though one suspects the insights gained would be as unsettling as they are illuminating. Consistency in methodological approach across different regulatory environments, and longer time horizons, represent further immediate needs.

Ultimately, this research is not an ending, but an invitation. An invitation to consider that even in the ostensibly ‘hard’ sciences of finance, language – and the way it shapes perception – is a non-negligible force. Future work should explore not only that sentiment matters, but how it is constructed, and the subtle cues that betray a firm’s true trajectory. Perhaps then, the shadows will begin to resolve into a clearer picture.

Original article: https://arxiv.org/pdf/2602.17851.pdf

Contact the author: https://www.linkedin.com/in/avetisyan/

See also:

- United Airlines can now kick passengers off flights and ban them for not using headphones

- Crimson Desert: Disconnected Truth Puzzle Guide

- All 9 Coalition Heroes In Invincible Season 4 & Their Powers

- Grey’s Anatomy Season 23 Confirmed for 2026-2027 Broadcast Season

- Mewgenics vinyl limited editions now available to pre-order

- Viral Letterboxd keychain lets cinephiles show off their favorite movies on the go

- Assassin’s Creed Shadows will get upgraded PSSR support on PS5 Pro with Title Update 1.1.9 launching April 7

- All Golden Ball Locations in Yakuza Kiwami 3 & Dark Ties

- Does Mark survive Invincible vs Conquest 2? Comics reveal fate after S4E5

- The Boys Season 5 Spoilers: Every Major Character Death If the Show Follows the Comics

2026-02-23 12:43