The US Securities and Exchange Commission (SEC), that tireless guardian of the common investor (or so they claim 🤔), has deigned to issue a statement. Not just any statement, mind you, but one of its most *definitive* yet, on the regulatory treatment of those digital trinkets we call stablecoins.

In a move that could reshape the market – or perhaps just shuffle the deck chairs on the Titanic – the agency, in its infinite wisdom, clarified that certain stablecoins, under conditions as specific as the diameter of a gnat’s nostril, do NOT fall under the definition of securities. Hallelujah! Or is it? 🤨

Tether Considers Shifting Strategy – A Retreat or a Feint?

The SEC, with the subtlety of a sledgehammer, labeled these assets as “covered stablecoins,” and they must meet requirements so strict, they’d make a Soviet breadline look lenient. All to remain outside the regulator’s… *benevolent* oversight.

“Covered Stablecoins are not marketed as investments; rather, they are marketed as a stable, quick, reliable and accessible means of transferring value, or storing value and not for potential profit or as investments,” the SEC declaimed. As if anyone *believes* that. We’re all just here for the “technology,” comrades! 🤪

According to the statement, a covered stablecoin must maintain a one-to-one peg with the US dollar and be backed by highly liquid, low-risk assets. Which, naturally, rules out anything remotely interesting.

It must also be redeemable on demand at full value. Importantly, these tokens cannot offer profit, interest, governance rights, or ownership stakes. Their sole function must be payment, money transfer, or value storage. Like a digital mattress stuffed with greenbacks that mysteriously lose value over time. 😴

The SEC explained that these assets are not investment vehicles and are typically marketed as “digital dollars.” As such, the agency does not consider its offer or sale to involve securities under federal law. How very generous of them. 🙄

“Accordingly, it is the Division’s view that Covered Stablecoins are not offered or sold as investment contracts,” the financial regulator concluded. Such certainty! Such confidence! One might almost believe it, if one hadn’t witnessed the agency’s *other* pronouncements.

This marks a rare moment of clarity from the SEC, which has often taken an ambiguous or enforcement-first approach to crypto regulation. Like a cat playing with a mouse, they occasionally offer a glimpse of escape before pouncing.

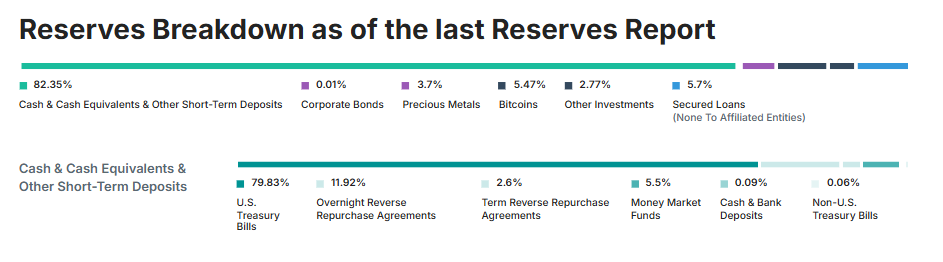

However, while the SEC’s guidance clearly provides a path forward for stablecoins like USDC, it casts a shadow dark as a Siberian winter on whether Tether’s USDT qualifies. The guidance specifically excludes reserves made up of crypto assets or precious metals, both of which are part of USDT’s current backing. A problem, you might say. A slight… *discrepancy*.

Meanwhile, Forbes journalist Nina Bambysheva reported that Tether is considering launching a new stablecoin to align with US regulations. This means the proposed asset would be fully backed by cash and US Treasuries. Such a pivot would mark a major shift in strategy for the issuer as it navigates increasing scrutiny. A shift as dramatic as a sudden turn in a blizzard.

Crypto analyst Novacula Occami also pointed out that USDT’s reserves include Bitcoin and gold, which are explicitly disqualified by the SEC’s criteria. As a result, USDT may fall within the scope of securities law and face potential restrictions in the US. A predicament worthy of Dostoyevsky!

“USDC and the Paxos coins comply with the SEC’s guidance and are not securities. USDT however, with its gold, BTC and other reserves are securities and cannot be legally offered in the US,” he added. A stark assessment, comrade. Brutal, but perhaps true. 🥶

Industry Reactions to the Regulator’s Move – A Chorus of Confusion?

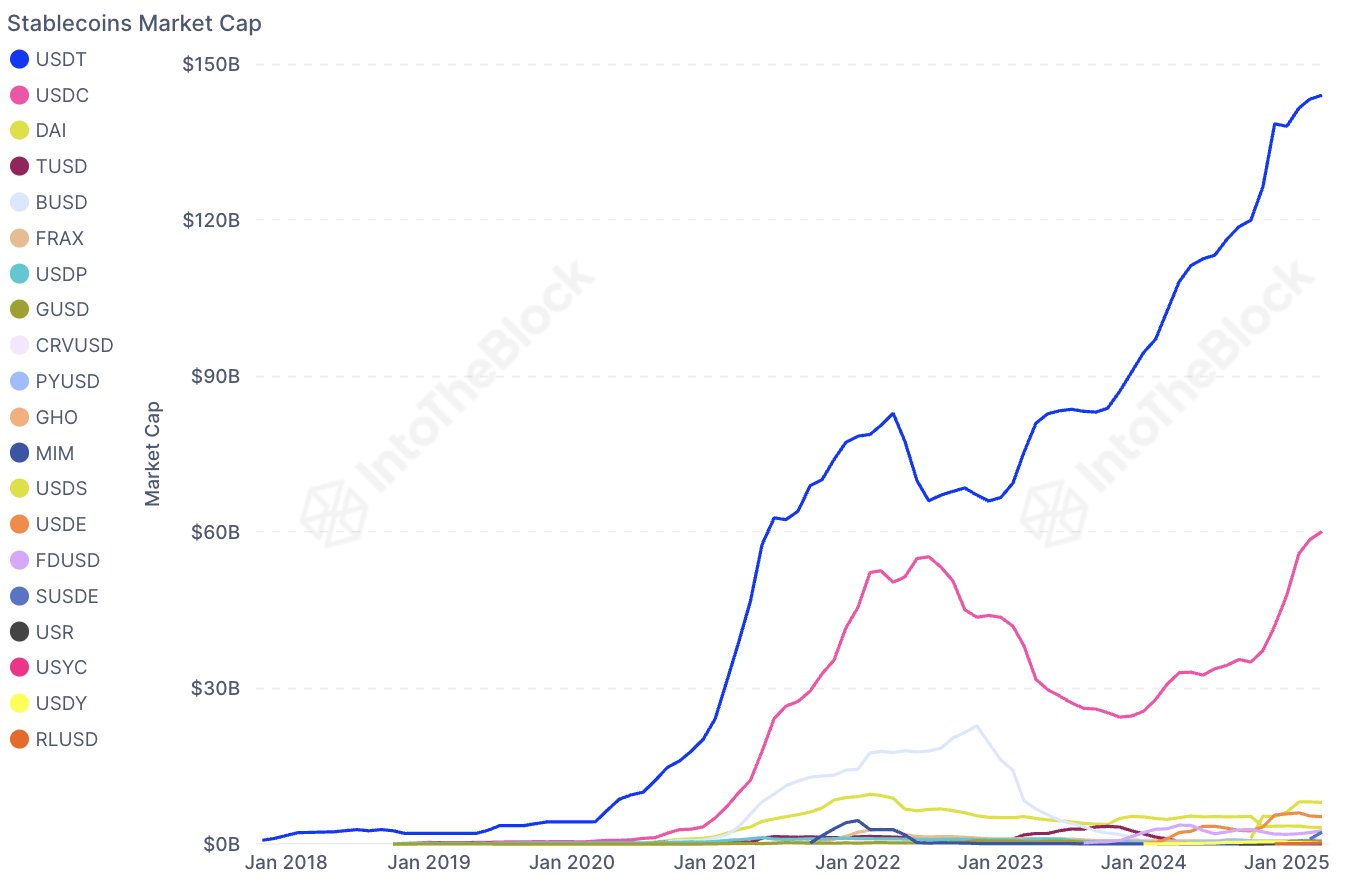

The news comes as stablecoins are gaining wider adoption despite market volatility. Daily usage continues to climb even during a challenging first quarter for digital assets. A flickering candle in the wind, perhaps, but a candle nonetheless.

Data from IntoTheblock shows that the sector increased by more than $30 billion during the first quarter of the year despite the broader market sell-off. A testament to the enduring allure of… something. Greed? Hope? Desperation? One can only speculate. 🧐

Nevertheless, industry responses to the new guidelines have been mixed. As predictable as the changing of the seasons.

David Sacks, a White House advisor on crypto policy, welcomed the move. Naturally. One hand washes the other, as they say.

Sacks said the statement provides long-overdue clarity and could ease regulatory burdens for compliant issuers. Assuming anyone *wants* to be compliant. The lure of the unregulated Wild West is strong, after all.

“The SEC has determined that fully-reserved, liquid, dollar-backed stablecoins are not securities. Therefore blockchain transactions to mint or redeem them do not need to be registered under the Securities Act,” Sacks stated. A victory for… someone. Perhaps the lawyers. 🤑

However, SEC Commissioner Caroline Crenshaw offered sharp criticism. There’s *always* one, isn’t there?

She warned that the guidance downplays risks in the stablecoin market and misrepresents key legal issues. A dissenting voice in the chorus. A whisper of truth in a sea of propaganda.

According to her, the statement presents an overly simplistic view of the industry. The SEC, simplistic? Never! Perish the thought! 🤣

“The [SEC’s] statement’s legal and factual errors paint a distorted picture of the USD-stablecoin market that drastically understates its risks,” Crenshaw added. A warning to heed, perhaps. Or to ignore at one’s peril. The choice, as always, is yours, comrade. 😈

Read More

- Who Is Harley Wallace? The Heartbreaking Truth Behind Bring Her Back’s Dedication

- 50 Ankle Break & Score Sound ID Codes for Basketball Zero

- Lost Sword Tier List & Reroll Guide [RELEASE]

- 50 Goal Sound ID Codes for Blue Lock Rivals

- 100 Most-Watched TV Series of 2024-25 Across Streaming, Broadcast and Cable: ‘Squid Game’ Leads This Season’s Rankers

- Umamusume: Pretty Derby Support Card Tier List [Release]

- Basketball Zero Boombox & Music ID Codes – Roblox

- KPop Demon Hunters: Real Ages Revealed?!

- The best Easter eggs in Jurassic World Rebirth, including callbacks to Jurassic Park

- Come and See

2025-04-05 13:32