Author: Denis Avetisyan

New research reveals that the architecture of stablecoins fundamentally shapes how systemic risk spreads during periods of market turbulence.

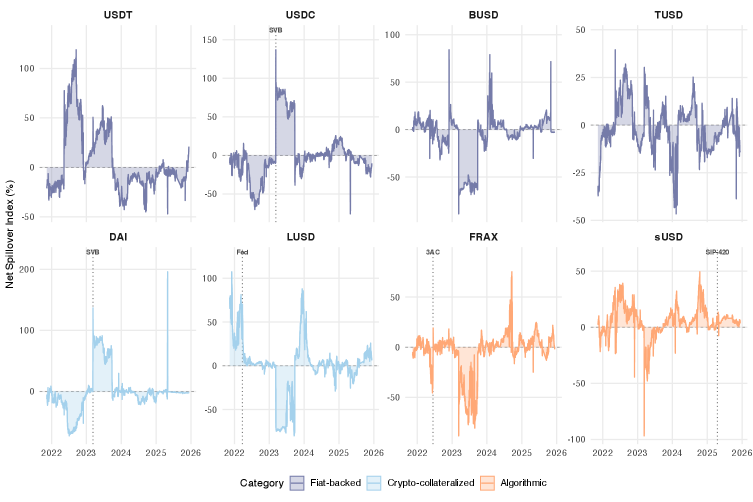

Analysis of quantile VAR models demonstrates that algorithmic and crypto-collateralized stablecoins amplify tail risk spillovers, while fiat-backed designs exhibit greater resilience.

Despite the promise of stablecoins to mitigate volatility in digital asset markets, their systemic risk implications remain poorly understood. This paper, ‘Stability Anchors and Risk Amplifiers: Tail Spillovers Across Stablecoin Designs’, utilizes Quantile Vector Autoregression and event studies to demonstrate that stablecoin design-specifically whether backed by fiat, crypto, or algorithms-fundamentally dictates their role in transmitting market stress. We find that while fiat-backed stablecoins act as ‘stability anchors’ with minimal spillover effects, algorithmic and crypto-collateralized designs amplify risk during extreme conditions, even as direct volatility channels emerge between traditional finance and crypto assets. Given these heterogeneous risk profiles, does a uniform regulatory approach to stablecoins adequately protect against future systemic shocks?

Navigating the Shifting Sands of Digital Value

Stablecoins have emerged as a pivotal component of the burgeoning cryptocurrency landscape, functioning as a crucial on-ramp and off-ramp between the volatile world of digital assets and the established financial system. These cryptocurrencies, designed to maintain a stable value often pegged to a fiat currency like the US dollar, facilitate seamless transactions and reduce the need for direct conversion to traditional currencies. This ease of use has driven rapid adoption, with stablecoin market capitalization experiencing substantial growth in recent years. Consequently, they now underpin a significant portion of cryptocurrency trading volume and are increasingly utilized in decentralized finance (DeFi) applications, effectively bridging the gap between traditional finance and the innovative, yet often complex, crypto ecosystem.

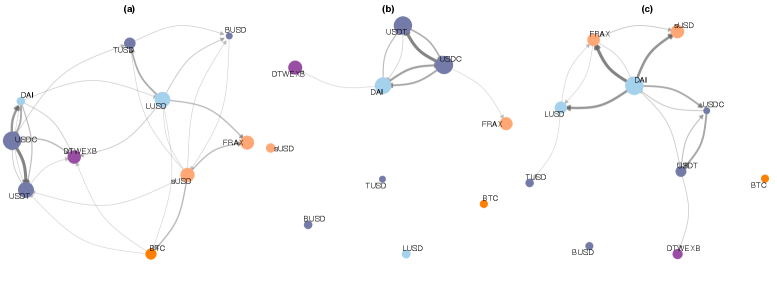

Stablecoins, while aiming for price stability, are far from uniform in their construction, and this diversity introduces a spectrum of systemic risks to the financial system. Designs range from those backed by traditional fiat currencies, held in reserve to maintain a one-to-one peg, to those relying on complex algorithms or other cryptocurrencies as collateral. The latter approaches, while innovative, create vulnerabilities stemming from feedback loops, collateral volatility, and the potential for ‘runs’ as confidence erodes. Critically, the interconnectedness within the crypto ecosystem means that instability in one stablecoin, particularly those with opaque or less-resilient designs, doesn’t remain isolated; it can rapidly propagate through decentralized finance (DeFi) protocols and traditional markets, impacting a wider range of assets and institutions. This complex interplay demands careful scrutiny of each stablecoin’s architecture to anticipate and mitigate potential contagion effects.

The interconnectedness of the crypto ecosystem means that instability in one stablecoin can rapidly propagate throughout the broader financial system. Recent analysis highlights the varying degrees of this risk, revealing that stablecoins relying on algorithms or crypto-collateralization are significantly more susceptible to spillover effects during periods of market stress. Specifically, these designs amplify potential negative consequences by 15 to 50 percentage points compared to stablecoins directly backed by fiat currency. This increased vulnerability stems from their reliance on internal crypto-assets, which are themselves prone to volatility, creating a feedback loop that exacerbates downturns and poses a substantial threat to systemic stability as the crypto market matures and integrates further with traditional finance.

Discerning Signal from Noise: Methodologies for Assessing Risk

Traditional correlation analysis, while commonly used to identify potential contagion effects between assets, is susceptible to inaccuracies stemming from heteroskedasticity – a condition where the variance of the errors is not constant across observations. This non-constant variance can inflate or deflate correlation coefficients, leading to spurious relationships or masking genuine ones. The Forbes-Rigobon Test directly addresses this limitation by employing a regression-based approach that accounts for differing volatility levels. Specifically, the test utilizes weighted least squares, assigning greater importance to observations with lower variance and mitigating the impact of heteroskedasticity on the estimated correlation. This results in a more reliable assessment of systemic risk and improved identification of true contagion pathways compared to standard Pearson correlation calculations.

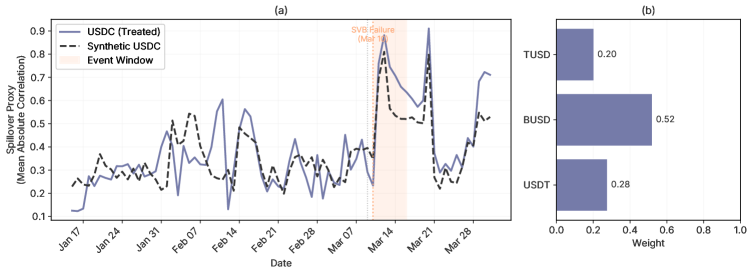

The Synthetic Control Method is a statistical technique used to estimate the causal effect of an intervention – such as the adoption or failure of a stablecoin – by constructing a counterfactual scenario. This involves creating a “synthetic” control group from a weighted combination of other units (e.g., other stablecoins or financial entities) that did not experience the intervention. The weights are determined by minimizing the difference in pre-intervention characteristics between the treated unit and the synthetic control, effectively replicating what would have likely happened to the treated unit in the absence of the intervention. This allows for a more robust assessment of impact than simple before-and-after comparisons, as it accounts for pre-existing trends and differences between the treated unit and the comparison group, mitigating selection bias and providing a more accurate estimate of the causal effect.

Accurate assessment of systemic vulnerability requires differentiating between genuine risk transmission and spurious correlations, a challenge addressed by employing robust statistical methodologies. Traditional correlation analysis can be misleading due to heteroskedasticity; however, techniques like the Forbes-Rigobon Test and the Synthetic Control Method offer more reliable insights. Specifically, a Synthetic Control analysis conducted regarding the SVB crisis and its potential impact on fiat-backed stablecoins yielded a p-value of 0.75. This result indicates that, statistically, there was no significant spillover effect from SVB exposure observed in the performance of these stablecoins, suggesting the initial contagion concerns were not substantiated by the data.

Deconstructing Stability: Sources of Vulnerability in Design

Fiat-backed stablecoins maintain their peg to a fiat currency, typically the US dollar, through the holding of reserve assets equivalent in value to the circulating supply of the stablecoin. The stability of these stablecoins is therefore directly dependent on Reserve Adequacy – the sufficiency, liquidity, and safety of those reserves. Crucially, transparency and verifiability of these reserves are paramount; regular audits and publicly available reports detailing the composition of the reserve portfolio are essential for building and maintaining market confidence. Without demonstrable proof of sufficient backing, fiat-backed stablecoins are vulnerable to bank runs and loss of peg, as users may lose faith in the issuer’s ability to redeem the stablecoin for the underlying fiat currency on demand.

Crypto-collateralized stablecoins utilize cryptocurrency as backing, often employing overcollateralization to mitigate risk; however, this introduces inherent leverage into the system. Because the stablecoin’s value is derived from a volatile asset, a decline in the collateral’s price can trigger liquidations. These liquidations are often executed by smart contracts to maintain the stablecoin’s peg, but can be self-reinforcing. As collateral value decreases, additional liquidations occur, potentially leading to a cascading effect where a large number of positions are forcibly closed in a short period. This systemic risk is amplified by the interconnectedness of decentralized finance (DeFi) protocols, where collateralized debt positions (CDPs) frequently interact, and can propagate instability throughout the ecosystem even if the initial price drop is relatively small.

Algorithmic stablecoins, distinct from their fiat- or crypto-collateralized counterparts, operate without reserve assets to back their value. This design relies entirely on code and market incentives to maintain a peg to a target price, typically the US dollar. When confidence in the algorithmic mechanism erodes-often triggered by negative market events or a lack of adoption-demand for the stablecoin decreases. The protocol then attempts to restore the peg by reducing the circulating supply, often through token burns or buybacks. However, if the loss of confidence is substantial, this contractionary process can accelerate, creating a self-reinforcing “death spiral” where price decreases further erode confidence, leading to more selling pressure and ultimately, a collapse in value. Unlike collateralized stablecoins which can absorb shocks through liquidation of reserves, algorithmic designs lack this buffer and are thus exceptionally vulnerable to rapid devaluation following a loss of trust.

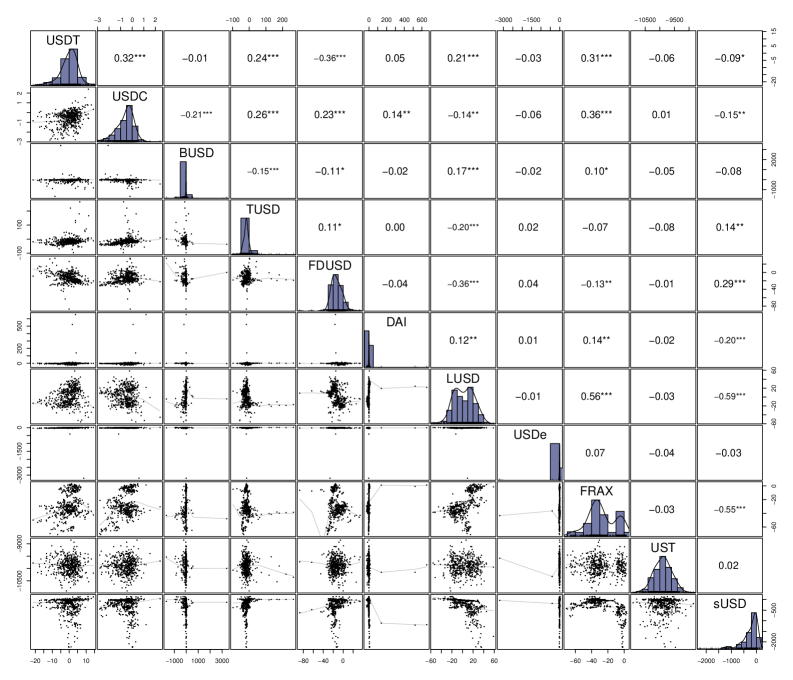

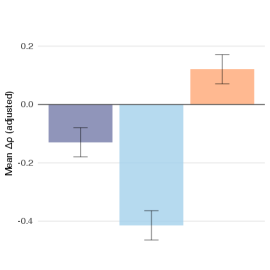

Analysis of the relationship between stablecoin performance and broader market indicators reveals differing stability characteristics based on collateralization design. Forbes-Rigobon adjusted correlation analysis indicates algorithmic stablecoins exhibit a positive correlation change of +0.07 with the US Dollar Index (DXY) and Bitcoin (BTC), suggesting a susceptibility to contagion – declines in one asset class directly correlate with declines in the stablecoin’s value. Conversely, both fiat-backed and crypto-collateralized stablecoins demonstrate negative correlation changes of -0.10 and -0.14 respectively. This suggests a flight-to-quality dynamic where investors move funds into these stablecoins during periods of DXY or BTC weakness, increasing demand and potentially bolstering their price stability.

The Ripple Effect: Market Dynamics and Amplification of Risk

Crypto markets are frequently characterized by volatility clustering, a phenomenon where periods of high price fluctuations tend to be followed by more of the same. This isn’t random noise; instead, prices exhibit a tendency to move in bursts, creating a self-reinforcing cycle of gains and losses. Such clustering significantly increases the probability of rapid and substantial price swings, which poses a particular threat to stablecoin systems. Because stablecoins are designed to maintain a fixed value, even short-lived periods of extreme market volatility can challenge their peg, potentially triggering a loss of confidence and a cascade of selling. The inherent interconnectedness of crypto assets means that volatility in one area can quickly spread, amplifying risks across the entire ecosystem and making stablecoins especially vulnerable during periods of heightened market stress.

The interconnectedness of the stablecoin ecosystem creates significant spillover effects, meaning instability in one digital asset can rapidly spread throughout the system and potentially impact traditional financial markets. Research indicates that a loss of confidence or a de-pegging event in a single stablecoin doesn’t remain isolated; instead, it triggers a cascade of selling pressure and diminished trust across similar assets. This propagation occurs due to shared backing assets, overlapping user bases, and the algorithms governing these digital currencies. Furthermore, the speed and efficiency of crypto trading exacerbate these effects, allowing risks to disseminate far more quickly than in conventional financial systems, potentially threatening broader market stability and necessitating careful monitoring of systemic risk.

Understanding the interconnectedness of stablecoin markets is now crucial for preventing broader financial instability. Research indicates that algorithmic and crypto-collateralized stablecoins significantly exacerbate the transmission of shocks – amplifying spillover effects in extreme market conditions by 15 to 50 percentage points when compared to stablecoins backed by fiat currency. This heightened sensitivity suggests that vulnerabilities within these crypto-asset dependent stablecoins pose a disproportionate risk to the wider financial ecosystem, demanding focused regulatory oversight and risk management strategies from both policymakers and market participants to preemptively address potential systemic failures.

The study of stablecoin designs reveals a predictable pattern: attempts to circumvent traditional financial structures introduce unforeseen vulnerabilities. The research demonstrates that algorithmic and crypto-collateralized stablecoins, while innovative, function as risk amplifiers during periods of market stress – a finding consistent with the inherent fragility of complex systems. As Niels Bohr observed, “The opposite of a trivial truth is also trivial.” This holds true here; the pursuit of decentralized stability, detached from established safeguards, doesn’t create resilience – it simply shifts the point of failure. The quantification of spillover effects across these designs underscores a crucial point: every metric is an ideology with a formula, and the illusion of control is often more dangerous than uncertainty itself.

What’s Next?

The observed divergence in systemic risk transmission across stablecoin designs isn’t particularly surprising – if one factor explained everything, it’d be marketing, not analysis. The finding that algorithmic and crypto-collateralized mechanisms amplify tail spillovers simply formalizes a suspicion long held by anyone familiar with the limitations of purely internal consistency. Future work must move beyond identifying that contagion occurs, and begin to rigorously model how it reshapes market fundamentals. Quantile VAR offers a useful diagnostic, but it’s a map, not the territory.

A pressing limitation remains the difficulty of isolating stablecoin-specific shocks. Disentangling spillover effects from broader macroeconomic trends – or, frankly, coordinated market manipulation – requires a level of high-frequency data and causal identification currently beyond reach. The field needs to embrace more granular stress-testing scenarios, moving beyond simple price shocks to incorporate liquidity crunches, oracle failures, and even reputational damage.

Predictive power is not causality. Demonstrating that certain designs correlate with increased risk doesn’t explain the underlying behavioral mechanisms. Are these amplified spillovers driven by rational herding, automated deleveraging, or simply the predictable collapse of unsustainable structures? Until that question is answered, stablecoin regulation will remain a game of whack-a-mole, addressing symptoms instead of systemic flaws.

Original article: https://arxiv.org/pdf/2602.18820.pdf

Contact the author: https://www.linkedin.com/in/avetisyan/

See also:

- United Airlines can now kick passengers off flights and ban them for not using headphones

- Crimson Desert: Disconnected Truth Puzzle Guide

- All 9 Coalition Heroes In Invincible Season 4 & Their Powers

- Mewgenics vinyl limited editions now available to pre-order

- Assassin’s Creed Shadows will get upgraded PSSR support on PS5 Pro with Title Update 1.1.9 launching April 7

- Grey’s Anatomy Season 23 Confirmed for 2026-2027 Broadcast Season

- Viral Letterboxd keychain lets cinephiles show off their favorite movies on the go

- Does Mark survive Invincible vs Conquest 2? Comics reveal fate after S4E5

- All Golden Ball Locations in Yakuza Kiwami 3 & Dark Ties

- Crimson Desert Guide – How to Pay Fines, Bounties & Debt

2026-02-24 14:13