President Donald Trump has nominated former Federal Reserve governor Kevin Warsh to lead the U.S. central bank, instantly reviving an old debate with real market consequences: Is Warsh a hard-money hawk, a quiet dove, or something closer to a modern-day Paul Volcker?

Why Kevin Warsh’s Fed Nomination Has Markets Nervous-and Divided

The answer matters, because investors are already trading the nomination as if Volcker himself just walked back into the Federal Reserve building. (Spoiler: He’s not. He’s probably at a beach in the Bahamas, sipping a margarita and judging us.)

Trump announced the nomination on Jan. 30, 2026, framing Warsh as a steady hand capable of restoring credibility and discipline at the Fed as Chair Jerome Powell’s term winds down in May. The timing is not subtle: Trump has repeatedly criticized the Fed’s rate posture and its independence, making Warsh’s policy instincts the central question. (Translation: “I don’t trust the Fed, so I’m going to appoint someone who’s basically a Fed version of a drama queen.”)

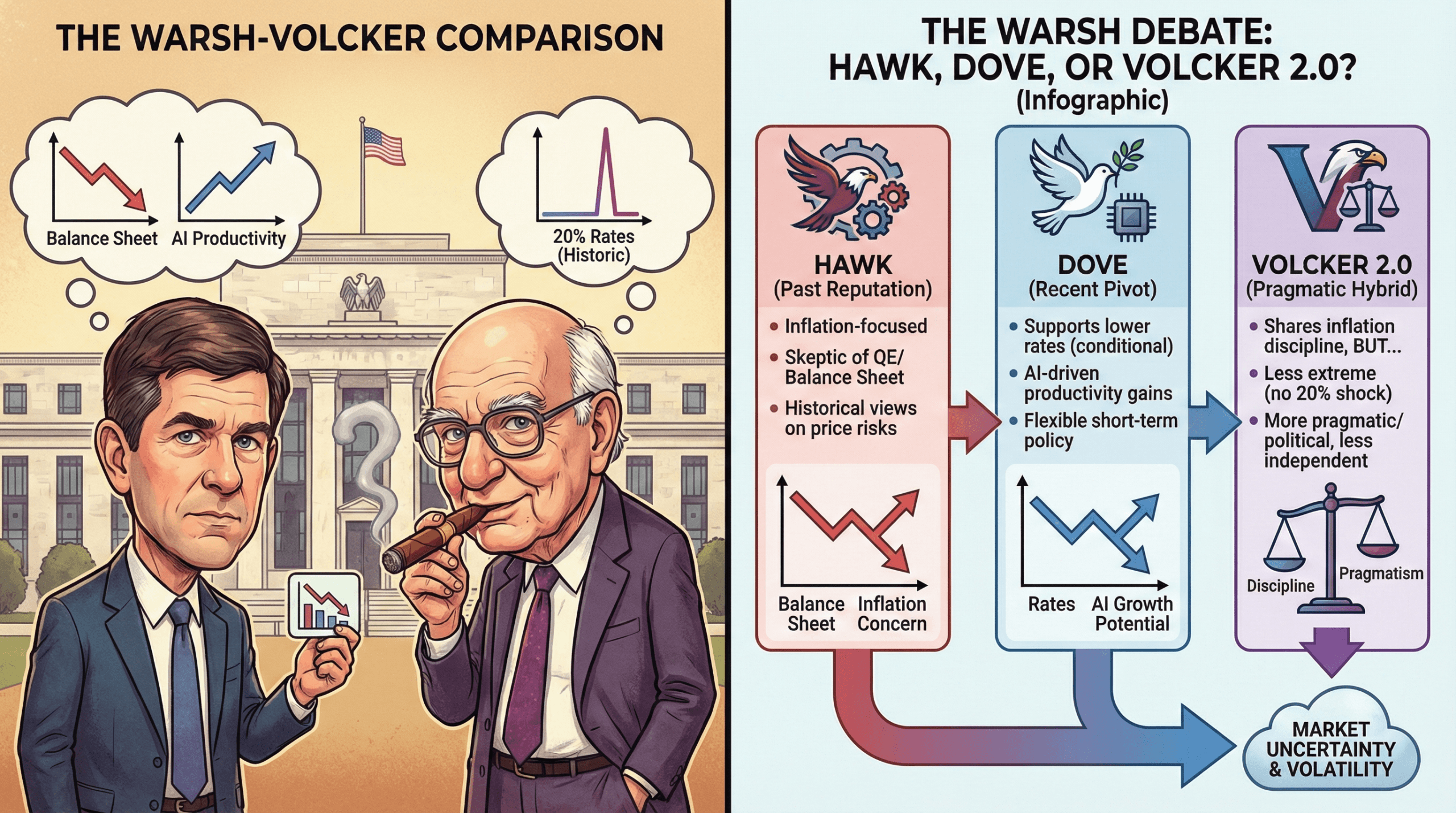

Warsh arrives with baggage-and receipts. As a Fed governor from 2006 to 2011, he earned a reputation as one of the most inflation-focused voices on the board, repeatedly flagging price risks even as the global financial crisis pushed unemployment higher and deflation fears spread. While others embraced aggressive easing, Warsh kept warning that inflation expectations could become unanchored. (Because nothing says “I’m a financial genius” like predicting inflation during a recession.)

At the time, Warsh said:

“ Inflation risks, in my view, continue to predominate as the greater risk to the economy.”

Those views hardened into a public philosophy after he left the Fed. Warsh became a sharp critic of quantitative easing (QE), calling the central bank’s swollen balance sheet a distortion that blurred the line between monetary and fiscal policy. He has repeatedly argued that inflation is not a mystery or a fluke, but the predictable outcome of excess spending and money creation. (Yes, even during a pandemic. Because obviously.)

“My overriding concern about continued QE, then and now, involves the misallocations of capital in the economy and the misallocation of responsibility in our government,” the Fed Chair nominee stated in 2018. (Translation: “I’m not saying the Fed is evil, I’m just saying they’re not as smart as I am.”)

That history explains why markets initially treated his nomination as a hawkish shock. Gold and silver sold off hard, the dollar firmed, and traders dusted off old Volcker comparisons. In short: the hard-money crowd smelled blood. (And also, apparently, a very strong coffee.)

But here’s where things get complicated. In recent years, Warsh has openly criticized Powell’s rate stance from the opposite direction-arguing that policy has become too restrictive and is holding back growth. He has said both interest rates and the Fed’s balance sheet should be lower, suggesting a willingness to cut rates if structural reforms do the heavy lifting. (Because nothing says “I’m a flexible thinker” like flipping your entire worldview based on a tweet from a president who hates you.)

That dual position-hawkish on balance-sheet discipline, flexible on short-term rates-has split analysts into camps. Some see intellectual consistency: shrink the Fed’s footprint and you earn room to ease. Others see political adaptation, particularly given Trump’s long-standing frustration with higher rates. (Because obviously, Warsh is just a puppet. Who knew?)

Volcker 2.0

This tension fuels the Paul Volcker comparison, but the resemblance has limits. Volcker, the 12th Chairman of the Federal Reserve, confronted runaway inflation in the late 1970s and responded by pushing the federal funds rate above 20%, willingly triggering a recession to restore credibility. Warsh has never faced that kind of inflationary inferno as chair, nor has he signaled a readiness to impose similar economic pain. (Because Volcker was a hero. Warsh is just… a guy with a spreadsheet.)

Volcker’s defining trait was independence. He resisted political pressure across administrations and let the consequences fall where they may. Warsh, by contrast, is widely viewed as more pragmatic-keenly aware of political realities and less inclined to wage war on the White House that appointed him. (Because nobody wants to be the Fed’s version of a disgruntled employee.)

That does not make him dovish. It makes him conditional. Warsh has consistently argued that inflation control is non-negotiable, but he also believes productivity gains-particularly from artificial intelligence-could allow for lower rates without reigniting price pressures. If that productivity story holds, he may look accommodative. If it cracks, the hawk likely reappears. (Because nothing says “I’m unpredictable” like a Fed chair who’s 50% economist and 50% conspiracy theorist.)

Markets seem undecided. Fed funds futures are pricing in additional rate cuts for 2026, even as traders brace for faster balance-sheet runoff. That combination hints at a hybrid Fed: tighter in structure, looser in signaling, and harder to pigeonhole. (Because nothing says “I’m confused” like a central bank that’s both a strict parent and a free-spirited hippie.)

If confirmed, Warsh may also revive an old-school Fed style-less forward guidance, fewer verbal crutches, and more emphasis on actions over promises. That alone could increase volatility, as markets adjust to a central bank that speaks less and surprises more. (Because nothing says “I’m a thrill-seeker” like a Fed chair who’s a mystery.)

So is Kevin Warsh a Volcker successor? Not quite. He shares Volcker’s skepticism of easy money and institutional sprawl, but not his appetite for economic shock therapy. Hawk or dove depends less on ideology than on conditions-and Warsh has made clear he intends to respond to data, not dogma. (Because who needs consistency when you can just wing it?)

For investors, the message is simple: ignore the labels. Warsh is neither a soft touch nor a crusader. He is a Fed chair nominee who believes inflation credibility matters-and who may prove more flexible than his reputation suggests. (Because nothing says “I’m a surprise” like a Fed chair who’s a walking contradiction.)

FAQ 🏦

- Is Kevin Warsh considered hawkish?

Yes, based on his long-standing emphasis on inflation control and opposition to prolonged quantitative easing. (But also, he’s a guy who once said “inflation is bad” during a depression. That’s not a stance, that’s a personality.) - Has Kevin Warsh supported lower interest rates?

Recently, yes-particularly if balance-sheet reductions and productivity gains offset inflation risks. (Translation: “I’ll cut rates if I feel like it, which is probably never.”) - Is Kevin Warsh comparable to Paul Volcker?

Only partially; he shares Volcker’s inflation discipline but lacks his record of extreme rate hikes and political independence. (Because Volcker was a superhero. Warsh is just… a guy with a coffee mug.) - How could Warsh change Fed policy if confirmed?

He may combine faster balance-sheet runoff with selective rate cuts and reduced forward guidance. (Because nothing says “I’m a boss” like a Fed chair who’s a master of ambiguity.)

Read More

- United Airlines can now kick passengers off flights and ban them for not using headphones

- Crimson Desert: Disconnected Truth Puzzle Guide

- All 9 Coalition Heroes In Invincible Season 4 & Their Powers

- Mewgenics vinyl limited editions now available to pre-order

- Grey’s Anatomy Season 23 Confirmed for 2026-2027 Broadcast Season

- Viral Letterboxd keychain lets cinephiles show off their favorite movies on the go

- The Boys Season 5 Spoilers: Every Major Character Death If the Show Follows the Comics

- Assassin’s Creed Shadows will get upgraded PSSR support on PS5 Pro with Title Update 1.1.9 launching April 7

- All Golden Ball Locations in Yakuza Kiwami 3 & Dark Ties

- Does Mark survive Invincible vs Conquest 2? Comics reveal fate after S4E5

2026-02-02 21:47