Author: Denis Avetisyan

New research reveals that financial transactions can be understood as random movements across networks, shedding light on the distribution of wealth and spending habits.

This study demonstrates that modeling financial transactions as random walks on activity-driven temporal networks reproduces observed heavy-tailed distributions of account balances and transaction sizes.

Understanding the circulation of money requires reconciling the complex interactions of individual economic agents with emergent, system-level properties. This is addressed in ‘Modeling financial transactions via random walks on temporal networks’, which proposes a framework representing financial transactions as random walks on activity-driven temporal networks. The model analytically derives heavy-tailed distributions for both account balances and transaction sizes, demonstrating that variance in individual spending propensity is a key driver of transaction patterns and reproduces observed correlations between inflows and outflows. Can this approach provide a more nuanced understanding of financial instabilities and inform strategies for mitigating systemic risk?

The Inherent Skew of Financial Landscapes

A robust depiction of financial systems necessitates a thorough understanding of how wealth and transactional activity are distributed amongst participants. Financial models often assume uniform distributions, but real-world data frequently reveals a markedly different picture: a skewed landscape where a small percentage of actors control a substantial portion of the resources and generate the majority of transactions. This unevenness isn’t merely a characteristic of wealth; it extends to activity levels, with a core group of users consistently engaging in a higher volume of financial exchanges. Consequently, accurately capturing these distributions – often described by Power-Law relationships – is paramount for creating simulations and analytical tools that reliably reflect the complexities of actual financial ecosystems and avoid systematic biases in forecasting or risk assessment.

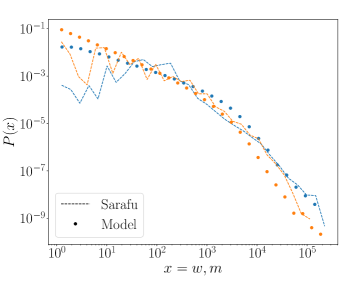

Analysis of financial networks consistently reveals an uneven distribution of wealth, frequently described by a Power-Law Decay. This principle, observed in both meticulously crafted simulations and real-world data from the Sarafu network, suggests that a relatively small percentage of accounts controls a substantial portion of the total funds. This isn’t simply a matter of statistical noise; the pattern indicates a fundamental characteristic of these systems, where wealth tends to concentrate rather than distribute evenly. Consequently, understanding this imbalance is crucial for modeling realistic financial ecosystems, as it significantly impacts the flow of transactions and the overall stability of the network. This concentration of funds necessitates a focus on the behavior of these ‘heavy hitters’ to accurately predict and potentially mitigate systemic risks.

The realistic simulation of financial networks hinges on capturing the inherent variability in how much money people transact at any given time. Traditional models frequently underestimate this variability, often assuming transactions follow a normal distribution, which fails to account for the occasional, but significant, large-value exchanges. This research demonstrates that Heavy-tailed distributions – where extreme values are more common than predicted by a normal curve – are not simply imposed as an assumption, but emerge from the natural variance in individual spending habits. By modeling each agent’s spending as a fluctuating variable, the simulation organically produces transaction sizes that align with observed real-world financial data, showcasing how micro-level behavioral differences can collectively generate macro-level systemic patterns and the potential for unexpectedly large transactions within a financial ecosystem.

Modeling the Flow: A Stochastic Framework

The fund transfer simulation utilizes a Random Walk model, where each transaction is represented as a discrete step between accounts. In this model, an agent randomly selects another agent to transfer funds to, with the probability of selection potentially weighted by network topology or other factors. The magnitude of each transfer is determined by pre-defined parameters or agent-specific characteristics. This stochastic process simulates the flow of money through the system, effectively modelling transactions as a series of random movements between accounts, allowing for observation of emergent patterns in fund distribution and velocity. The model doesn’t predict specific account-level outcomes, but rather provides statistical insights into the overall dynamics of fund transfer within the defined system.

The stochastic model operates under a strict principle of fund conservation, meaning the total amount of money within the simulated system remains constant throughout the duration of the simulation. This is enforced by ensuring every fund transfer from one account to another is a zero-sum transaction; any monetary value leaving an account is precisely matched by an equivalent increase in the receiving account’s balance. Consequently, the model does not introduce external capital or remove existing capital; all observed changes in account balances are strictly the result of internal redistribution of a fixed monetary supply. This constraint is crucial for maintaining the validity of the simulation and ensuring that any observed dynamics are attributable to the agent behaviors and transfer probabilities, rather than artificial inflation or deflation of the overall system wealth.

The spending propensity of each agent within the fund transfer model is quantified as a probability, p_i, representing the likelihood that agent i will initiate a fund transfer during a given time step. This value, assigned to each agent, directly influences transaction rates; higher p_i values correlate with more frequent transfers initiated by that agent. The overall transaction dynamics are therefore a function of the distribution of these spending propensities across the agent population; a population with generally high propensities will exhibit a greater volume of transactions compared to a population with lower values. Furthermore, variations in spending propensity contribute to heterogeneity in transaction patterns, impacting the speed and efficiency of fund distribution throughout the simulated network.

Asset-exchange models, originating in physics, conceptualize fund transfers as analogous to the kinetic exchange of particles. In this framework, each account represents a state and fund transfers represent collisions, conserving the total ‘mass’ (total funds) within the system. The probability of a transfer between two accounts is determined by parameters akin to collision cross-sections, defining the likelihood of interaction. This approach allows for the application of statistical mechanics and kinetic theory to analyze the emergent behavior of the fund transfer network, moving beyond individual transaction details to focus on aggregate properties like fund velocity and distribution. \text{Total Funds} = \sum_{i=1}^{N} A_i , where A_i represents the funds held by account i, and remains constant throughout the simulation, reflecting the principle of fund conservation.

Capturing the Nuances of Spending Behavior

The Binomial Distribution serves as a base model for quantifying the number of random walks originating from each node within the network. This distribution calculates the probability of observing a specific number of successes (random walks) in a fixed number of trials, assuming each trial is independent and has a constant probability of success. In this context, each node is considered a potential origin for a random walk, and the probability of a walk originating from a given node is determined by its inherent attractiveness or activity level. The Binomial Distribution is defined by two parameters: n, representing the number of trials (potential random walks), and p, representing the probability of success (a random walk originating from that node). While foundational, this model assumes homogeneity across nodes, which is not reflective of real-world spending patterns, necessitating the use of more complex distributions like the Beta-Binomial.

The Beta-Binomial distribution addresses limitations of the Binomial distribution when modeling spending behavior by accounting for overdispersion. While the Binomial distribution assumes a fixed probability of success (spending) for each agent, real-world data exhibits greater variance than this model predicts. This increased variance arises from the fact that agents are heterogeneous; they do not all have the same propensity to spend. The Beta-Binomial distribution models this heterogeneity by allowing the probability of success to vary randomly across agents, following a Beta distribution. Specifically, the probability p is not fixed, but rather a random variable drawn from a Beta(\alpha, \beta) distribution, effectively weighting the Binomial distribution with a prior reflecting the distribution of individual spending propensities. This results in a distribution with a higher variance than the Binomial, better capturing the observed overdispersion in empirical spending data.

Spending events are not typically distributed uniformly over time; instead, they exhibit periods of high activity followed by relative inactivity, a phenomenon known as burstiness. To model this, we employ the Weibull distribution, characterized by two parameters: a scale parameter λ which governs the typical duration of inactive periods, and a shape parameter k that determines the degree of burstiness. A lower k value indicates a higher propensity for bursty behavior, meaning more frequent, concentrated spending events. The Weibull distribution allows for a flexible representation of inter-event times, capturing the observed tendency for spending to cluster rather than occur at regular intervals, and provides a more realistic depiction of agent behavior than Poisson processes which assume constant rates.

The Activity-Driven Network is constructed by leveraging the statistical distributions of individual spending behavior – specifically the Beta-Binomial and Weibull distributions – to determine node activity levels. This activity then dynamically influences the probability of interaction between nodes; higher activity increases the likelihood of connection. Validation of this approach demonstrates successful recovery of the empirically observed Joint activity-attractiveness distribution, indicating the model accurately reflects the relationship between a node’s engagement and its desirability as a connection point within the network. This recovery is achieved through comparing the modeled distribution with observed data, confirming the model’s capacity to represent real-world spending patterns and network dynamics.

Bridging Theory with Real-World Finance

The presented modeling approach finds concrete application within the realm of community-based finance through analysis of the Sarafu digital currency dataset. This unique system, designed to facilitate local economies and mutual aid, offers a compelling case study for examining the dynamics of financial networks beyond traditional banking structures. Sarafu operates as a peer-to-peer digital currency, primarily used within a network of small businesses and individuals, and provides a rich source of transactional data reflecting real-world economic interactions. By applying network analysis to Sarafu’s transaction history, researchers can gain insights into how value flows within a localized, community-driven financial ecosystem, and validate the model’s ability to capture the characteristics of such systems – moving beyond purely theoretical simulations.

Empirical validation of the modeling approach is made possible through access to the transaction data from the Sarafu digital currency, which is publicly available via the UK Data Service. This resource provides a comprehensive record of financial interactions within a real-world, community-based economic system, allowing researchers to move beyond simulations and test the model’s predictive power against observed data. The availability of this detailed transactional history is crucial for confirming the model’s ability to accurately capture the complex dynamics of financial networks, and for identifying any discrepancies between theoretical predictions and actual economic behavior. Access to such a robust and openly available dataset fosters transparency and reproducibility in the research, enabling further investigation and refinement of the model.

Financial transactions are not isolated events; they unfold over time, creating a dynamic web of interactions. Recognizing this, the study employs a Temporal Network structure, which explicitly accounts for the timing of each transaction. Unlike traditional network analyses that treat all connections as simultaneous, this approach captures how relationships evolve and change based on when interactions occur. This is crucial for understanding financial systems like Sarafu, where the sequence of payments and the duration of relationships significantly impact trust, liquidity, and overall system stability. By modeling the network as a time-varying entity, the research gains insight into patterns of financial behavior that would be obscured in a static representation, revealing how the flow of value changes over time and influencing the resilience of the community-based financial system.

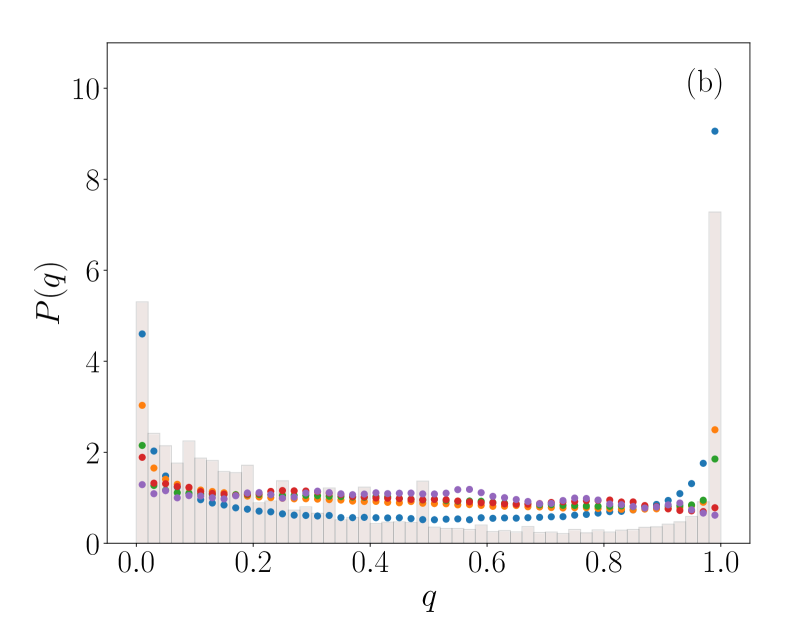

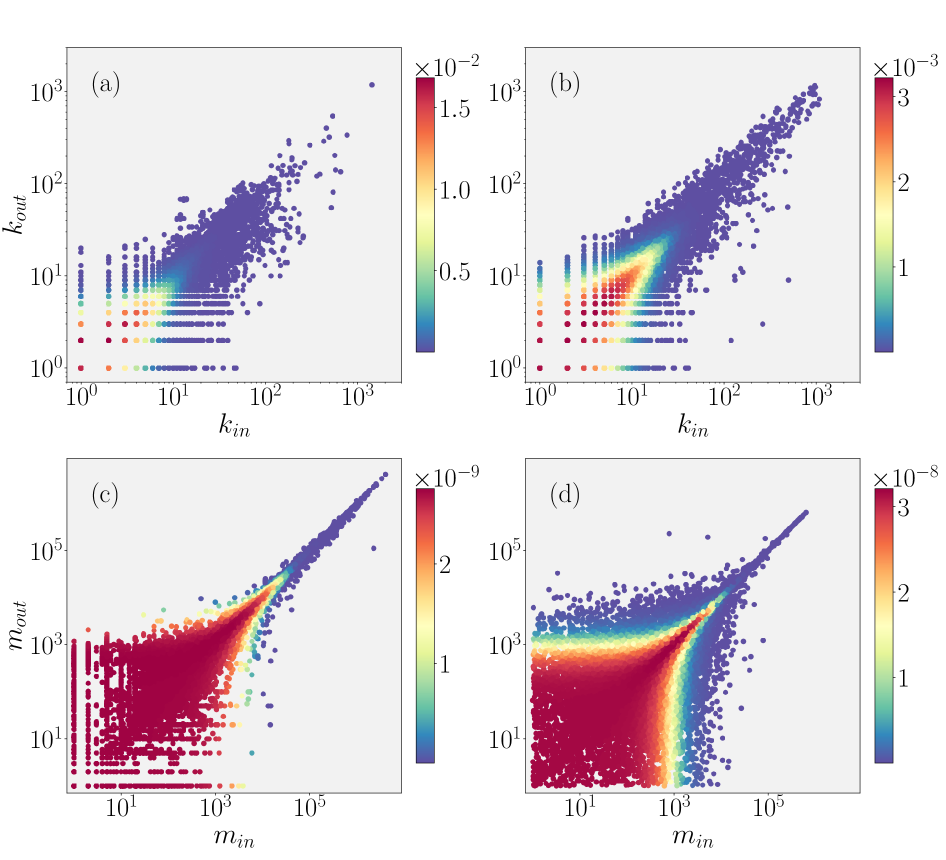

Analysis of the Sarafu digital currency dataset reveals a striking consistency between modeled financial interactions and real-world economic behavior. Specifically, both the distribution of account balances and the sizes of individual transactions follow a Power-law decay, indicating that a small number of actors hold a disproportionately large share of the currency, and a few large transactions account for a significant portion of the total economic activity. This pattern, also observed in the simulated data, suggests fundamental principles governing the flow of value within this community-based financial system. Further bolstering this observation, the correlation between a user’s incoming and outgoing transactions-essentially, who sends money to whom-also demonstrates a Power-law decay, revealing a self-organizing structure in the network of financial exchanges and hinting at the presence of influential nodes within the Sarafu ecosystem.

The study of financial transactions, as presented in this work, reveals a fascinating parallel to the natural world’s tendency towards entropy. The modeling of these exchanges as random walks on temporal networks isn’t simply a mathematical exercise; it’s an acknowledgement that systems, even those seemingly governed by rational actors, inevitably diffuse and redistribute value over time. Stephen Hawking once observed, “The best way to predict the future is to understand the past.” This sentiment resonates deeply with the approach taken here; by analyzing the patterns of past transactions-the ‘walks’ taken on the network-researchers gain insight into the future distribution of wealth and the inherent dynamics of economic systems. The observed heavy-tailed distributions aren’t flaws in the model, but rather symptoms of a system learning to age gracefully, a natural consequence of activity-driven networks and individual spending behavior.

What Lies Ahead?

The successful mapping of financial exchange onto the framework of random walks on temporal networks offers a compelling, if provisional, harmony. It is a rare phase of temporal harmony when a model so neatly captures the observed distributions of wealth and transaction size. However, to mistake this alignment for a lasting stability would be unwise. The model, as presented, remains largely descriptive; a faithful mirroring of observed phenomena rather than a predictive engine. The inherent complexities of human economic behavior-the irrational exuberance, the panicked retrenchment-are currently absorbed into the stochasticity of the walk itself.

Future iterations must move beyond this. The true challenge lies in identifying the underlying mechanisms that shape the network’s activity, not merely documenting its patterns. What biases influence the probabilities governing these random walks? Are there emergent properties of the network structure-feedback loops, preferential attachment, or cascading failures-that contribute to the observed heavy tails? This is not simply a matter of refining parameters; it is a question of understanding the forces that drive the system toward increasing imbalance.

Like all infrastructure, this modeling approach will accrue technical debt. The elegance of the current framework cannot indefinitely mask the need for greater realism-the incorporation of heterogeneous agents, regulatory constraints, or even behavioral biases. The model’s longevity will depend not on its initial fidelity, but on its capacity to age gracefully, adapting to the inevitable erosion of its simplifying assumptions.

Original article: https://arxiv.org/pdf/2602.20713.pdf

Contact the author: https://www.linkedin.com/in/avetisyan/

See also:

- United Airlines can now kick passengers off flights and ban them for not using headphones

- Crimson Desert: Disconnected Truth Puzzle Guide

- All 9 Coalition Heroes In Invincible Season 4 & Their Powers

- Mewgenics vinyl limited editions now available to pre-order

- Grey’s Anatomy Season 23 Confirmed for 2026-2027 Broadcast Season

- Viral Letterboxd keychain lets cinephiles show off their favorite movies on the go

- Assassin’s Creed Shadows will get upgraded PSSR support on PS5 Pro with Title Update 1.1.9 launching April 7

- How to Get to the Undercoast in Esoteric Ebb

- The Original Resident Evil is Finally Available on Steam

- All Golden Ball Locations in Yakuza Kiwami 3 & Dark Ties

2026-02-25 06:39