Strategy, a priggish debutante formerly known as MicroStrategy, announces a further offering of perpetual preferred stock, professing to soothe the nerves of those who tremble at the volatility of its humble common shares, as the CEO deigns to declare.

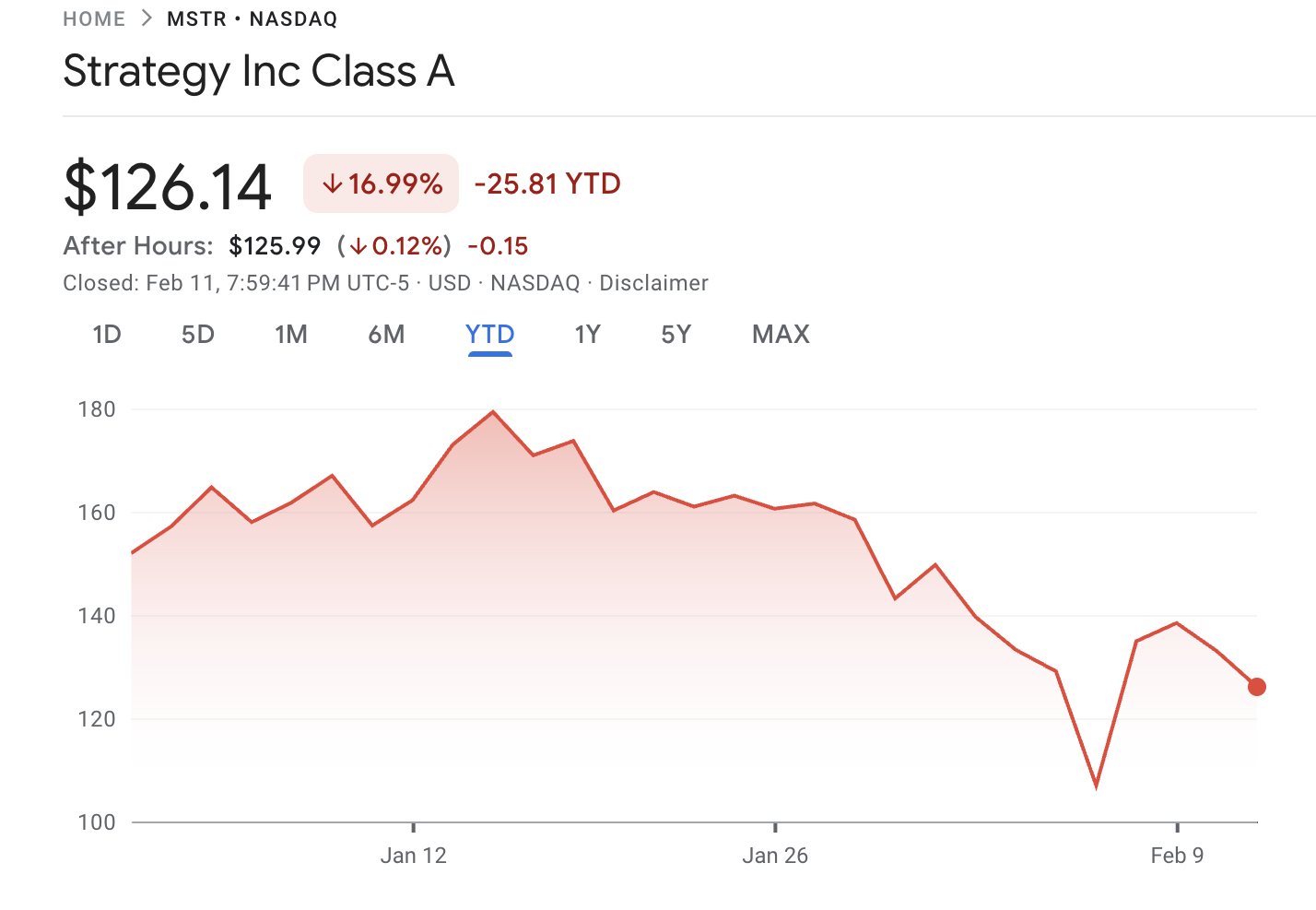

The proclamation lands on a stage where Strategy’s stock, known by the badge MSTR, has sagged by roughly 17% thus far this year.

The CEO Claims Stretch May Become Strategy’s Principal Means of Funding

In a recent chat with Bloomberg, Strategy’s CEO Phong Le addressed Bitcoin‘s capricious temperament. He argued its volatility stems from its very essence-a digital flirtation with fate. When BTC ascends, Strategy’s digital asset treasury plan makes its ordinary shares theatrically rise; when it falls, the shares fall with dramatic gusto.

Conversely, during downturns, the shares tend to decline more sharply. He noted that Digital Asset Treasuries (DATs), including Strategy, are engineered to follow the leading cryptocurrency.

To address this dynamic, the company is promoting its perpetual preferred shares, branded “Stretch.”

“We’ve engineered something to protect investors who long for digital capital without that volatility, and that something is Stretch,” Le told Bloomberg. “For me, the story of the day is Stretch closing at $100, exactly as it was engineered to perform.”

The preferred shares offer a variable dividend, currently set at 11.25%, with the rate reset monthly to encourage trading near the $100 par value.

One must not pretend that this is the main theatre of Strategy’s capital-raising. The company sold about $370 million in common stock and a mere $7 million in perpetual preferred shares to fund its previous three weekly Bitcoin purchases.

Nevertheless, Le said, Strategy is actively educating investors about what preferred shares can do.

“We are educating the faithful about the wonders of preferreds,” he admitted. “A touch of seasoning, a dash of marketing, and a great deal of patience. This year the liquidity of our preferreds has flirted with 150 times that of other peers; Stretch shall become a venerable product, and we shall gradually retire equity to let preferred capital take the stage.”

MicroStrategy’s Bitcoin Bet Under Pressure With Shares Trading Below Net Asset Value

The plot thickens as Strategy’s usual finance of the coin grows more brittle under pressure. The firm continues to amass Bitcoin, adding over 1,000 BTC in a week, and now sits on 714,644 BTC.

Yet Bitcoin’s price slip has pressed down on Strategy’s balance sheet like a stealthy chandelier. With coins near $67,422, well below Strategy’s average price of about $76,056, the unrealized loss stands around $6.1 billion.

The common stock has mirrored this tragedy, dropping 5% on a single Wednesday; year-to-date, MSTR slides about 17%, while the Bitcoin draught has lost over 22% so far.

As prior declared, Strategy’s accumulation of Bitcoin leans on equity issuance. A sly measure is the mNAV-the multiple to net asset value-gauging how the share price mimes the Bitcoin behind each share.

According to SaylorTracker, Strategy’s diluted mNAV hovers around 0.95x, a gentle reminder that the stock trades at a discount to the Bitcoin backing per share.

That discount complicates the performance of the play: when shares adorn themselves above NAV, new stock can be issued, more Bitcoin purchased, and possibly create value for shareholders; when trades dip below NAV, further issuance risks diluting them, like chorus girls losing their footing.

Thus Strategy tilts toward perpetual preferred stock, a fashionable hat on its capital structure, designed to sustain Bitcoin acquisitions while attempting to allay the crowds’ anxieties about volatility and valuation’s tempests.

For MSTR shareholders, the shift may lower the dilution risk: less common equity issuance means fewer pearls ripped from the necklace of value, and perhaps a gentler preservation of Bitcoin per share and the thud of discounted issuances.

Yet the move carries a grim accessorising: higher fixed dividend obligations that threaten to bow the budget if Bitcoin remains recalcitrant. The plan alters the risk silhouette rather than banishing the very volatility tied to its Bitcoin treasury.

Read More

- United Airlines can now kick passengers off flights and ban them for not using headphones

- Gold Rate Forecast

- How to Solve the Glenbright Manor Puzzle in Crimson Desert

- How to Get to the Undercoast in Esoteric Ebb

- 8 Actors Who Could Play Blackbeard In One Piece Live-Action Season 3

- All Golden Ball Locations in Yakuza Kiwami 3 & Dark Ties

- How to Complete Bloom of Tranquility Challenge in Infinity Nikki

- Blind Tekken 8 player reaches one of the game’s highest ranks after two years of grinding

- $2B AI cow collars use “cowgorithm” to herd cattle with no fences

- All MLB The Show 26 Quirks & What They Do

2026-02-12 08:51