Nakamoto Holdings, that Bitcoin-native conglomerate started by David Bailey, the BTC Inc. CEO (because who doesn’t want to start a company with that much responsibility?), just dumped around $20 million worth of Bitcoin. And guess what? They took a whopping 40% loss on it. Yes, you read that right. The kind of loss that says, “Oh no, this wasn’t part of the plan.” Apparently, they bought the BTC at around $33,000 per coin and sold at what we’ll call market value, which is less than stellar.

Now, this wasn’t some casual rebalancing-because who needs to sell at a 40% loss on something they were supposed to be all-in on? A company whose entire identity is based on accumulating BTC selling at a loss? Yeah, something’s off here. This screams urgency. The kind of urgency that you don’t see in textbooks about ‘sound financial strategies.’

And get this: they raised over $750 million in 2025 with the grand plan of holding Bitcoin forever (or so it seemed). Now they’re selling for a loss, and naturally, people are wondering if they forgot the whole “liquidity management” thing when they were drafting their strategy. Awkward.

Bitcoin treasury company Nakamoto Inc. (NASDAQ: NAKA) disclosed in its 10-K filed on March 30, 2026, that it sold approximately 284 BTC in March for about $20 million, with an average selling price of around $70,422 per BTC. In 2025, the company net purchased 5,342 BTC with a…

– Wu Blockchain (@WuBlockchain) March 30, 2026

Here’s the kicker: Nakamoto merged with KindlyMD, a healthcare provider, in May 2025, raising a solid $510 million PIPE, plus some debt financing to boot. Their model was supposed to be foolproof. Or, at least, that’s what the paperwork said. Basically, they wanted to keep cycling BTC gains back into… more Bitcoin, while holding back just 40% in public equity. But whoops, selling at a loss totally didn’t fit the whole ‘insulated against liquidation’ part of the plan. Someone didn’t read the fine print.

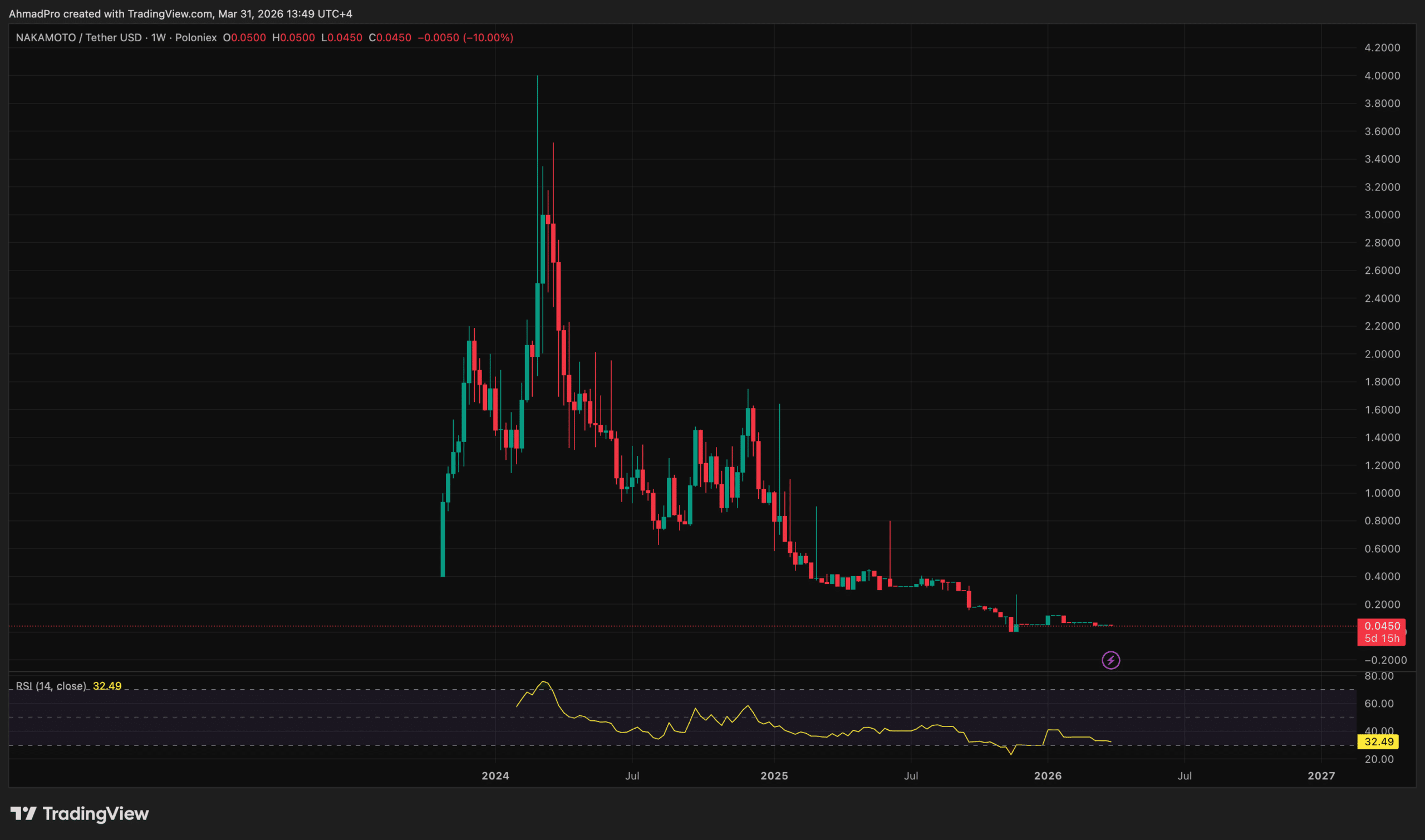

Implied Acquisition Cost vs. Realized Exit Price For Nakamoto Bitcoin Holdings

If we do the math (don’t worry, we’ll do it for you), a 40% loss on $20 million means Nakamoto paid around $33.3 million for that chunk of Bitcoin. So, in the end, they got back about $0.60 for every dollar they thought they were going to make. Ouch.

Now, if this sale happened when Bitcoin was hitting those lovely highs of $80,000 to $95,000, this would mean Nakamoto was buying at a crazy $133,000 to $158,000 per coin. That’s some bold purchasing strategy right there-basically a “buy high, sell low” situation that no one would advise. But here we are.

David Bailey’s $NAKA and Cory Klippsten’s $SQNS duking it out to see who can lose the title of worst managed BTCTC

– Pledditor (@Pledditor) March 30, 2026

And no, we still don’t know exactly how this sale went down-whether it was an OTC block trade, on the open market, or a ‘just get rid of it’ kind of exchange liquidation. The trail’s gone cold, as it were.

But here’s the one thing we do know: this wasn’t some tiny little tax-loss move on the side. A $13.3 million loss? That’s a real gut punch for a company that was all about long-term Bitcoin holding. And it just highlights a structural flaw in their approach: buying Bitcoin near market peaks with expensive capital? Not the best move when the market decides to, you know, not go your way.

EXPLORE: Crypto breakout alerts this week

Balance Sheet Pressure and What the Liquidation Reveals

Here’s how Nakamoto’s funding model was supposed to work: issue equity or notes at a premium, buy BTC, let the BTC appreciate, and poof-you’ve got a growing treasury. Simple, right? Well, that works as long as the stock price doesn’t tank. Guess what? It did. By early 2026, Nakamoto’s stock had crashed by 99% from its May 2025 highs. So now, instead of leveraging equity, the company is left with just cash reserves and liquidation options. Which, as you can guess, involves selling BTC at a massive loss.

Source: Tradingview

Meanwhile, other BTC treasury firms have taken different approaches. MSTR doubled down and raised more capital (because why not, right?), while GameStop, the rogue hero, stuck to its guns, holding onto its 4,710 BTC. They could afford that because they don’t have the debt obligations. Nakamoto? Not so much. They’re cashing out to stay afloat.

And don’t even get me started on governance. Nakamoto’s acquisition of Bailey’s other businesses-BTC Inc. and UTXO Management-while the stock price was in free fall? Some people are calling it self-dealing. But hey, it’s all in the name of innovation, right?

So there you have it: a Bitcoin treasury firm, selling at a loss, while acquiring its founder’s companies. What a show.

DISCOVER: Best Memecoins To Buy This Month!

Read More

- United Airlines can now kick passengers off flights and ban them for not using headphones

- All Itzaland Animal Locations in Infinity Nikki

- How to Complete Bloom of Tranquility Challenge in Infinity Nikki

- Katanire’s Yae Miko Cosplay: Genshin Impact Masterpiece

- How to Get to the Undercoast in Esoteric Ebb

- Crimson Desert: Disconnected Truth Puzzle Guide

- Gold Rate Forecast

- Superman/Spider-Man #1 Review: Bigger DC-Marvel Crossovers Teased

- A Dark Scream Theory Rewrites the Only Movie to Break the 2-Killer Rule

- All Golden Ball Locations in Yakuza Kiwami 3 & Dark Ties

2026-03-31 14:37