Quick Facts (Because Who Doesn’t Love a Good List of Financial Hype? 🤡):

- 💰 1️⃣ Over $8.3B in real-world assets are already tokenized on-chain and growing fast. (Seriously, who knew tokenizing a government bond could be so exciting?)

- 🏦 2️⃣ Banks like Goldman Sachs and BNY Mellon are integrating blockchain custody for Treasuries and money-market funds. (Because nothing says “trust us” like putting your money on a blockchain that’s still figuring out how to handle basic math.)

- 🚀 3️⃣ $HYPER, $BEST, and $LINK are well-positioned to benefit from the next phase of tokenization. (Or, as I like to call it, “the future of finance, but with more confusion.”)

- 🔄 4️⃣ The shift from DeFi vs. TradFi to DeFi + TradFi marks a new era in digital finance. (Because nothing says “innovation” like a bank and a blockchain finally realizing they’re both just trying to steal your money.)

Crypto’s been around for nearly two decades, and in that time, we’ve seen narratives change. From “Bitcoin will replace banks” to “Wait, maybe banks can help us?” It’s like watching a soap opera, but with more blockchain. 🧵

Way back in the beginning, DeFi (decentralized finance) and TradFi (traditional finance) were supposed to be competitors. DeFi would grow and develop into a rival financial system, providing all the advantages that TradFi lacked: transparency, accountability on the blockchain, natively-digital assets, and more. 🤯

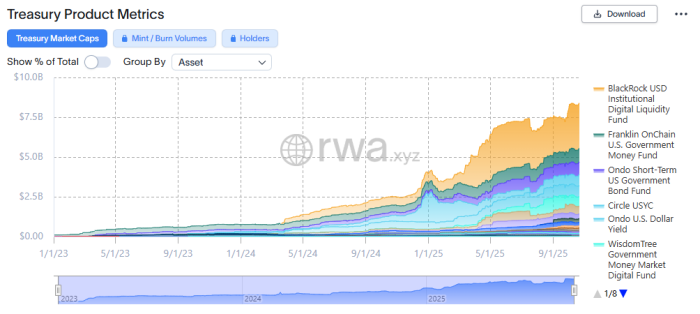

That’s not what we see today. Instead, TradFi looked around, saw DeFi – and liked what it saw. Now, big banks and financial institutions are adopting crypto left, right, and center – and tokenized assets lead the way, particularly tokenized US treasuries, long since a favorite tool of the financial system. 🏦

According to recent figures, approximately $8.3B in Treasuries have already been tokenized on-chain, with broader estimates putting the total closer to $24-30B. (Because nothing says “we’re serious” like turning government debt into a digital puzzle.)

For years, institutions such as Goldman Sachs and BNY Mellon shunned crypto custody, citing regulatory and accounting burdens. Today, they are tokenizing money-market funds, short-term government debt and other liquid assets that naturally fit the blockchain model. (Because nothing says “we’re modern” like a bank using a technology that’s still called “crypto.”)

The logic is operational rather than speculative: tokenized funds enable corporate treasurers to move cash faster, pledge assets more flexibly and settle trades outside the usual cut-off times. (Or, as I like to call it, “The Future of Finance, But With Less Sleep.”)

If you’re a large, multi-national corporation moving large volumes of cash and securities, those benefits are highly appealing. (Unless you’re a human, in which case, enjoy your existential dread.)

But tokenization requires custody – holding both the underlying assets (the treasuries themselves, for instance) and the resulting tokens. That’s where the story gets interesting, as the race for custody heats up. 🏃♂️💨

Crypto-native firms like Coinbase, with $246B in assets under custody, and Fidelity Investments currently dominate crypto asset custody, charging fees in the order of 0.05 %-0.15% of asset value. (Because nothing says “we’re in this together” like a 0.15% fee.)

As tokenized assets scale, those fee revenues add up; if tokenized cash and Treasuries continue to grow from $8B now to reach $25-40B, annual revenues of $300-600M would flow into crypto custodians. (Because nothing says “profit” like a blockchain that’s still figuring out how to count.)

Coinbase has the crypto knowledge and infrastructure, but banks already have the client base, trust relationships and regulatory permissions to hold large balance sheets. If they can integrate tokenization into existing custody services, they could capture a major part of that value chain. (Because nothing says “disruption” like a bank finally catching up to the 2010s.)

Tokenization is growing at a phenomenal rate. In 2024 alone:

- 📈 Total market cap of tokenized assets increased by 32% (Because who needs a stable economy when you can have 32% growth in something that’s still a mystery?)

- 📈 Tokenized treasuries surged by 179% (Because nothing says “we’re excited” like a 179% increase in government debt.)

- 📉 Private credit grew 40% (Wait, that’s not a typo. It’s 40% growth in private credit. Because who needs a recession when you can have 40% growth in something that’s still a mystery?)

- 📉 Commodities increased 5% (Because nothing says “we’re thrilled” like a 5% increase in commodities.)

Each of those categories is expected to report even greater growth in 2025. (Because nothing says “optimism” like a 2025 forecast that’s already a stretch.)

As tokenization booms and banks turn their eyes towards crypto, what are the best crypto to buy now? Look for $HYPER, $BEST, and $LINK to potentially grow by 10x or more as tokenization takes root. (But remember, if you lose all your money, it’s not my fault. I warned you about the “tokenization” part.)

1. Bitcoin Hyper ($HYPER) – Canonical Bridge to Bitcoin’s Layer-2 Next Chapter 🚀

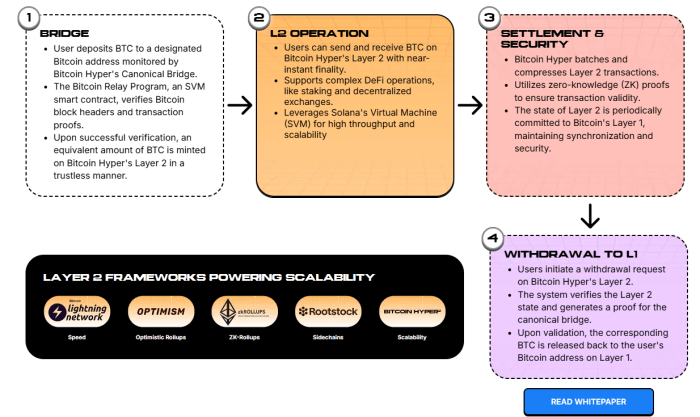

Bitcoin Hyper ($HYPER) serves as a next-generation Layer-2 scaling solution that merges the security of Bitcoin with the high-speed architecture of the Solana Virtual Machine (SVM). (Because who doesn’t want their Bitcoin to be faster than a toddler on a sugar rush?)

Designed with a Canonical Bridge, it enables $BTC to be wrapped, staked, and transacted on a high-throughput Layer 2, allowing near-instant payments, DeFi integration, and complex smart contracts. (Because nothing says “we’re serious” like a blockchain that’s also a magic trick.)

What is $HYPER? A next-level advance that addresses Bitcoin’s two greatest limitations: transaction speed and network congestion, and lack of scalability. (Because nothing says “we’re solving problems” like a blockchain that’s still figuring out how to handle basic math.)

By introducing ZK-based validation and cross-chain consensus, it unlocks thousands of transactions per second while maintaining a cryptographic link to the Bitcoin mainnet. (Because nothing says “security” like a blockchain that’s still figuring out how to count.)

Holders can stake $HYPER to earn yield, participate in governance, and use their $BTC in DeFi ecosystems for the first time at scale. (Because nothing says “democracy” like a blockchain that’s still figuring out how to handle voting.)

With over $24M raised in its presale, Bitcoin Hyper is emerging as one of 2025’s most anticipated projects, with nearly $25M raised so far. Our $HYPER price prediction expects Bitcoin Hyper could reach $0.20 by the end of 2026, up 1,425% over the current price of $0.013155. (Because nothing says “hope” like a 1,425% increase in a token that’s still a mystery.)

Learn how to buy Bitcoin Hyper and visit the presale page to learn more. (But don’t say I didn’t warn you.)

2. Best Wallet Token ($BEST) – Non-Custodial Wallet Ready for Tokenization 🛡️

Best Wallet ($BEST) powers a non-custodial, multi-chain Web3 wallet built for the current wave of crypto adoption and tokenization. (Because nothing says “trust me” like a wallet that’s also a multi-chain party.)

The platform integrates DeFi, token swaps, NFT storage, and advanced crypto presale access within a single mobile interface. It’s a potent combo of user-friendly simplicity with advanced on-chain functionality. (Because nothing says “convenience” like a wallet that’s also a Swiss Army knife.)

The $BEST token drives the wallet’s reward ecosystem, offering staking APY, governance rights, and launchpad access for early-stage token sales. (Because nothing says “power” like a token that’s still figuring out how to handle rewards.)

The project’s roadmap emphasizes interoperability across Ethereum, BNB Smart Chain and Solana networks. (Because nothing says “future-proof” like a blockchain that’s still figuring out how to talk to itself.)

More chains will be added as the project grows. Users can also leverage Best Wallet’s multi-wallet capacity to create up to five individual wallets within the app, allowing them to group tokens according to blockchain. (Because nothing says “organization” like a wallet that’s still figuring out how to manage multiple accounts.)

As self-custody and digital-asset security gain mainstream attention, $BEST is positioned to become the utility backbone of a wallet ecosystem. The presale, currently at $16.6M, offers tokens for $0.025835. (Because nothing says “value” like a token that’s still figuring out how to price itself.)

That $BEST price is predicted to rise to $0.072 by the end of the year, delivering 178% gains for current investors. (Because nothing says “profit” like a 178% increase in a token that’s still a mystery.)

Visit the Best Wallet Token presale page for the latest information. (But don’t say I didn’t warn you.)

3. Chainlink ($LINK) – Oracles that Power DeFi and TradFi Adoption 🌐

Chainlink ($LINK) is rapidly transitioning from being a leading blockchain oracle network to a pivotal bridge between legacy finance and decentralized systems: (Because nothing says “connection” like a blockchain that’s still figuring out how to talk to itself.)

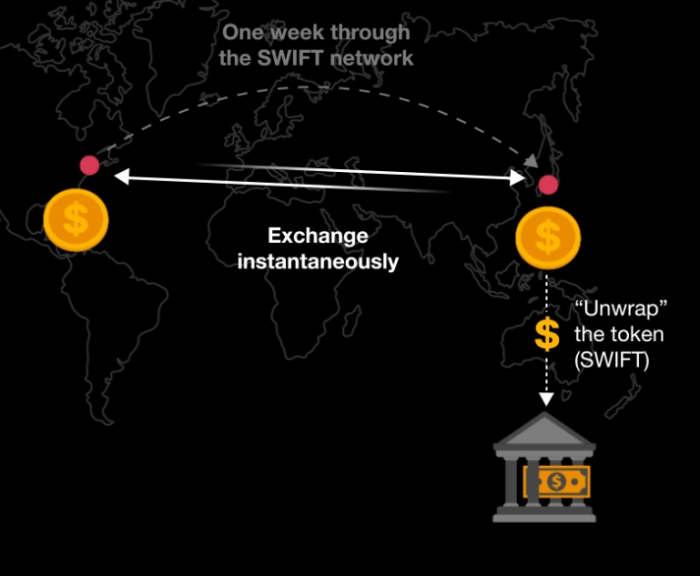

- 🤝 Chainlink collaborated with SWIFT to allow banks to continue using ISO 20022 message formats, while triggering on-chain events via Chainlink’s architecture, meaning institutions can keep familiar processes and rails while adopting tokenized finance. (Because nothing says “compatibility” like a blockchain that’s still figuring out how to handle legacy systems.)

- 🔐 Chainlink also introduced the ‘Digital Transfer Agent’ (DTA) technical standard, which enables fund administrators and custodians to manage tokenized fund subscriptions and redemptions in the same way they do today – but now on-chain. (Because nothing says “efficiency” like a blockchain that’s still figuring out how to handle paperwork.)

- 🤝 A major initiative with 24 global financial institutions, including DTCC and Euroclear, aims to standardize corporate-actions data on-chain and streamline asset-servicing operations. (Because nothing says “progress” like a blockchain that’s still figuring out how to handle data.)

Chainlink explicitly links their own development to asset tokenization. At a recent conference, founder Sergey Nazarov demonstrated just how big the potential market is: (Because nothing says “ambition” like a blockchain that’s still figuring out how to scale.)

Markets worth hundreds of trillions are all in play – and Chainlink intends to open them all to crypto. (Because nothing says “confidence” like a blockchain that’s still figuring out how to handle trillions.)

What’s happening with TradFi and DeFi may appear incremental. Tokenizing money-market funds isn’t flashy. But the underlying implication is profound: banks are positioning to become the custodians and operational backbone of the next generation of digital finance. (Because nothing says “revolution” like a blockchain that’s still figuring out how to handle basics.)

The flows of tokenized assets – not just the headline amounts – will determine who controls balance sheets of the future, and $BEST, $LINK, and $HYPER are all poised to play active roles. (Because nothing says “influence” like a blockchain that’s still figuring out how to handle power.)

As always, do your own research. This isn’t financial advice. (But if you do lose everything, it’s not my fault. I warned you about the “tokenization” part.)

Authored by Bogdan Patru for Bitcoinist – https://bitcoinist.com/best-crypto-to-buy-now-as-crypto-rwa-hits-8-3-billion

Read More

- United Airlines can now kick passengers off flights and ban them for not using headphones

- The Boys Season 5 Spoilers: Every Major Character Death If the Show Follows the Comics

- Solo Leveling’s New Manhwa Chapter Revives a Forgotten LGBTQ Story After 2 Years

- Grok’s ‘Ask’ feature no longer free as X moves it behind paywall

- Assassin’s Creed Shadows will get upgraded PSSR support on PS5 Pro with Title Update 1.1.9 launching April 7

- Invincible Season 4 Episode 6 Release Date, Time, Where to Watch

- TikToker’s viral search for soulmate “Mike” takes brutal turn after his wife responds

- All 9 Coalition Heroes In Invincible Season 4 & Their Powers

- Mewgenics vinyl limited editions now available to pre-order

- All Itzaland Animal Locations in Infinity Nikki

2025-10-23 16:47