Author: Denis Avetisyan

A new network analysis reveals the complex web of connections driving volatility and spillover effects among Chinese real estate firms during the ongoing crisis.

This study employs network analysis and variance decomposition to quantify connectedness and volatility transmission within China’s real estate sector, with a focus on the role of state ownership.

Despite increasing scrutiny of systemic risk, understanding contagion dynamics within complex financial ecosystems remains challenging. This is addressed in ‘Volatility Spillovers in China’s Real Estate Crisis: A Network Approach’, which utilizes a network analysis to map the transmission of volatility among major Chinese real estate developers during the ongoing crisis. The study reveals how investor sentiment and regional exposures shaped connectedness patterns, demonstrating a shift from shared systemic shock to localized vulnerabilities and, ultimately, a pricing-in of risk as the crisis matured. How will these evolving spillover effects reshape investment strategies and regulatory oversight in China’s property sector moving forward?

Unveiling Fragility: Patterns in China’s Real Estate Landscape

For decades, China’s real estate sector fueled an unprecedented economic boom, becoming integral to the nation’s growth and a key indicator of its financial health. However, this foundation is now demonstrably fragile, as evidenced by the mounting financial difficulties of industry giants like Evergrande and Country Garden. These developers, once symbols of China’s prosperity, are grappling with immense debt burdens and liquidity issues, triggering concerns about systemic risk within the broader economy. The struggles aren’t isolated incidents; they represent a wider pattern of overleveraging, speculative investment, and slowing demand that threatens to destabilize a sector previously considered impervious to downturns. The current instability marks a significant departure from the consistent growth experienced over the past several decades, prompting both domestic and international observers to reassess the long-term trajectory of China’s economic model.

China’s attempts to rein in excessive borrowing within its vast real estate sector, most notably through the ‘Three Red Lines’ policy, have yielded unintended consequences. Intended to limit developer debt by capping levels relative to assets, cash flow, and liability, the policy effectively cut off crucial funding sources for many companies. This restriction on capital access, while aiming for long-term stability, swiftly triggered liquidity issues and defaults, particularly amongst heavily indebted developers. The resultant inability to complete projects eroded investor confidence, creating a feedback loop of declining property values and increased financial risk. Consequently, a policy designed to mitigate systemic risk inadvertently accelerated the current crisis, demonstrating the complex interplay between regulatory intervention and market dynamics within the Chinese property landscape.

A palpable decline in investor confidence is actively deepening the challenges within China’s real estate sector, establishing a detrimental feedback loop. As apprehension grows regarding developer solvency and future property values, investment slows, directly contributing to further price declines. This erosion of value, in turn, reinforces initial fears, accelerating the withdrawal of capital and increasing the potential for widespread financial risk. Notably, the scale of this investor network-measured by transaction volumes and market participation-has demonstrably contracted during periods of negative news, such as developer defaults, but experienced brief expansions coinciding with government interventions or optimistic economic indicators, revealing a highly sensitive and volatile market dynamic.

Mapping Interdependence: Observing Systemic Connections

A vector autoregression (VAR) model was utilized to statistically quantify interrelationships in the stock returns of selected real estate developers. This multivariate time series model treats the returns of each developer as endogenous variables, allowing for the assessment of reciprocal influences. To address potential multicollinearity and improve model parsimony, Elastic Net regularization was incorporated. Elastic Net combines L1 (Lasso) and L2 (Ridge) regularization techniques, penalizing both the magnitude and number of coefficients, thereby identifying the most salient relationships while preventing overfitting. The resulting VAR model provides estimates of the direct and indirect impacts of one developer’s stock performance on the others, facilitating the measurement of systemic risk within the sector.

The Vector Autoregression (VAR) model incorporates rolling window estimation, a technique wherein the model is repeatedly estimated over a moving time window. This approach allows for the capture of time-varying relationships between developer stock returns, accommodating non-stationary data and evolving systemic risk. Specifically, the rolling estimation facilitates observation of changes in network size – the total number of developers exhibiting significant interdependencies – and node positions, reflecting alterations in the relative influence and vulnerability of individual firms within the network. The window size and update frequency are critical parameters, balancing responsiveness to recent changes with the need for statistical stability in the estimated coefficients.

Analysis demonstrates substantial financial interconnectedness among real estate developers, evidenced by the rapid transmission of shocks between firms. Initially, these spillover effects are largely attributable to shared regional economic exposures; a negative shock to one developer in a specific geographic area impacts others operating in the same market. However, the drivers of these spillovers evolve over time, shifting towards firm-specific characteristics as the analysis progresses, indicating that idiosyncratic risks and financial linkages between individual companies become increasingly important in propagating financial distress within the network.

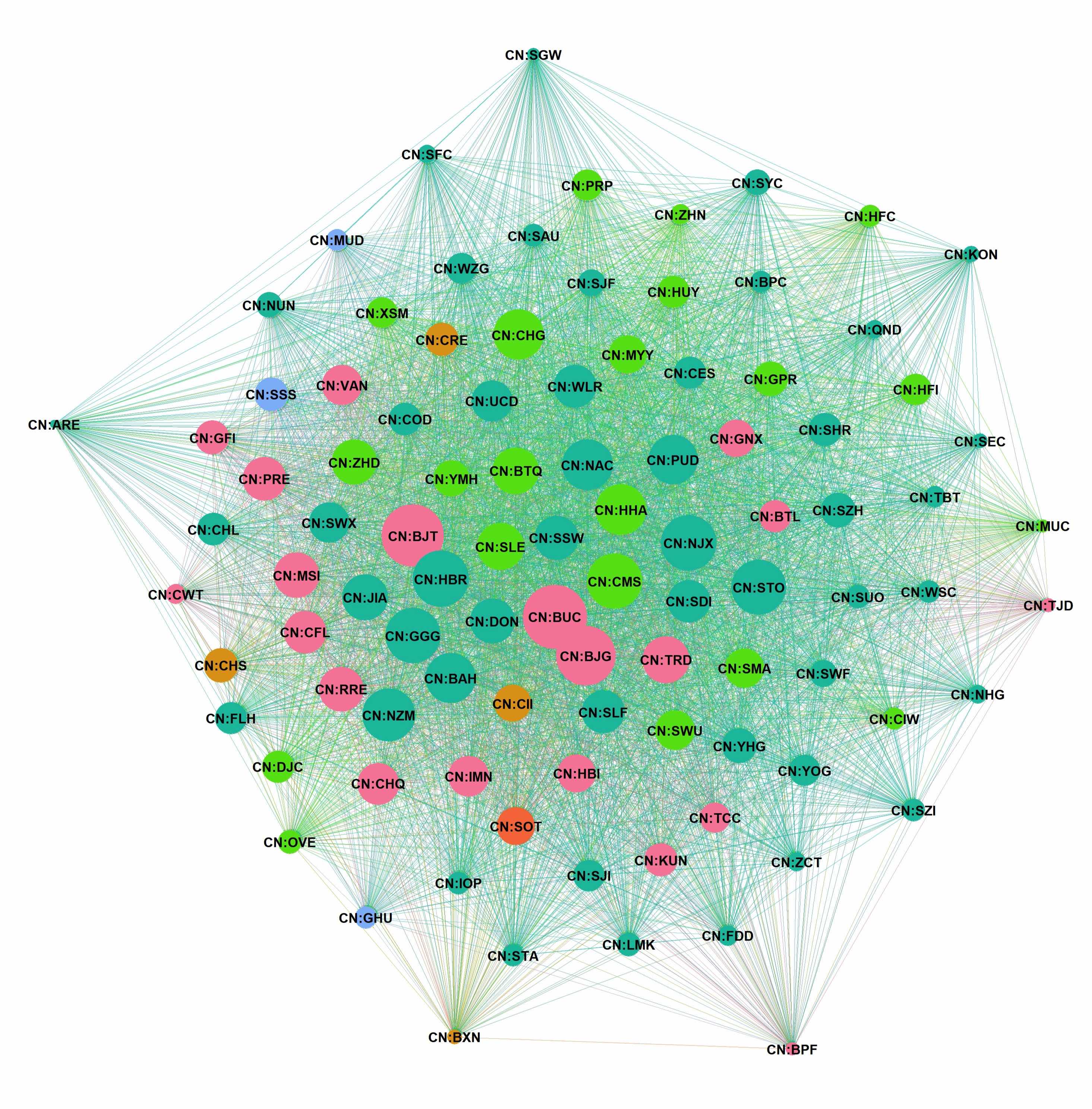

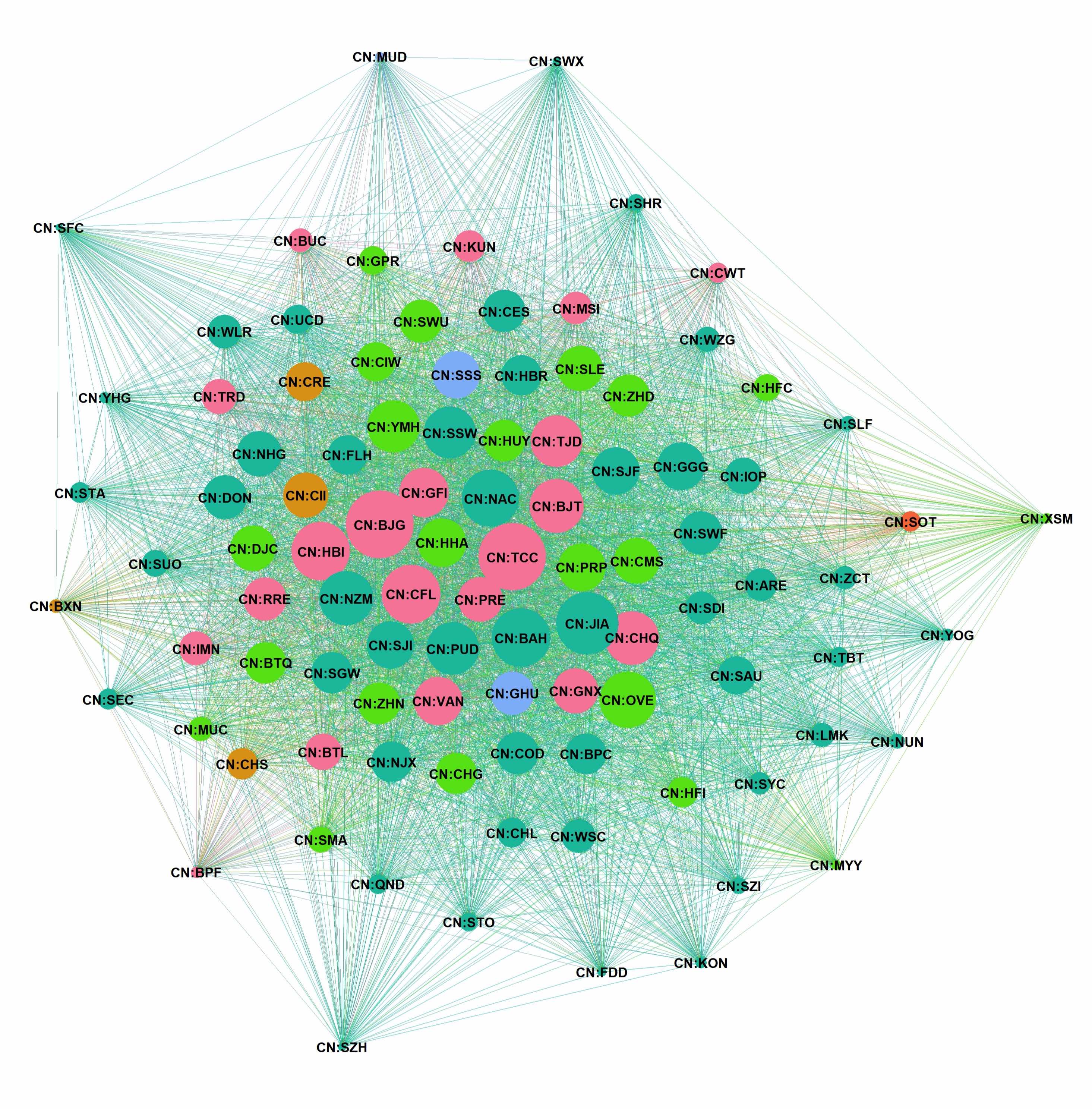

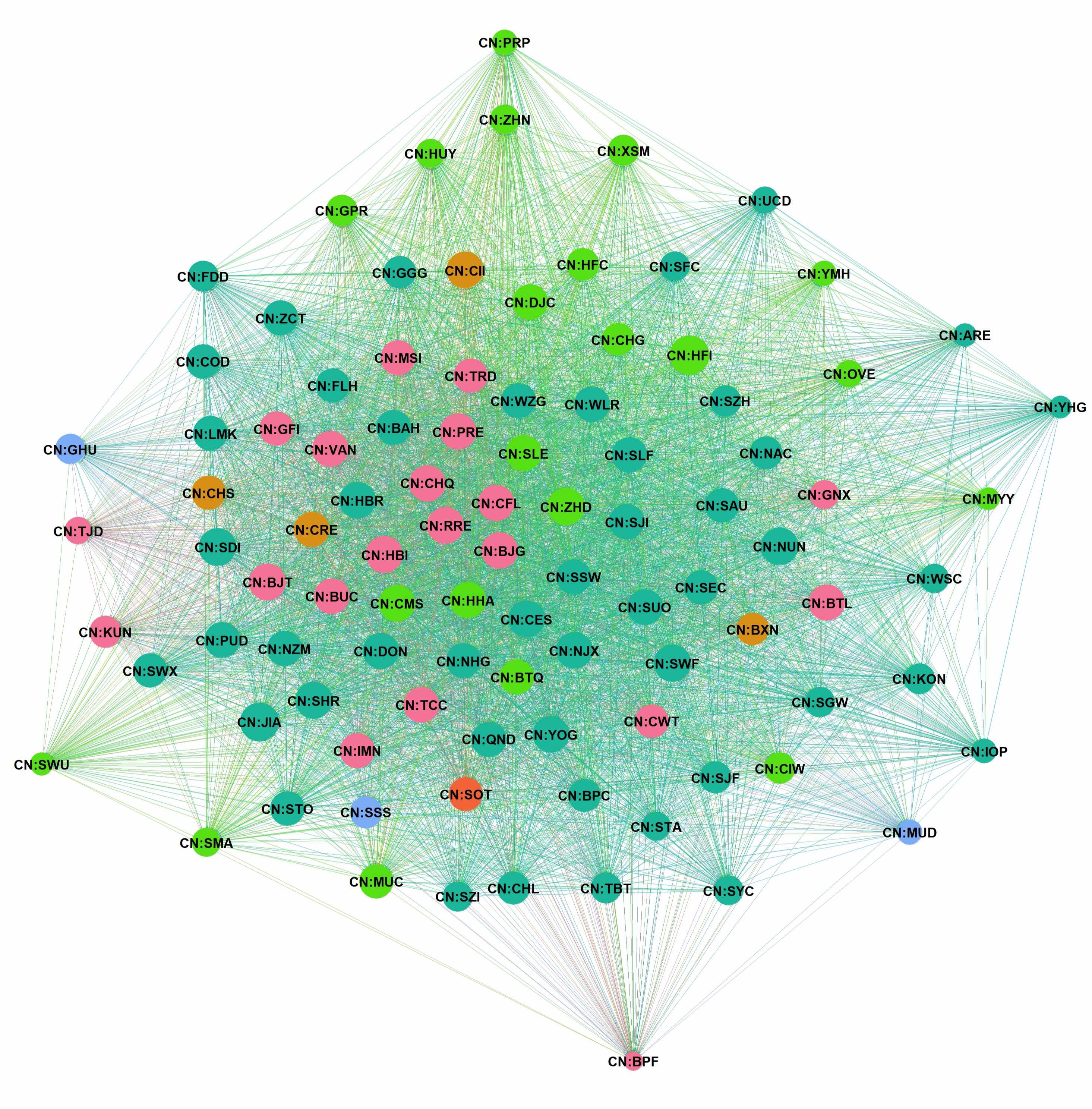

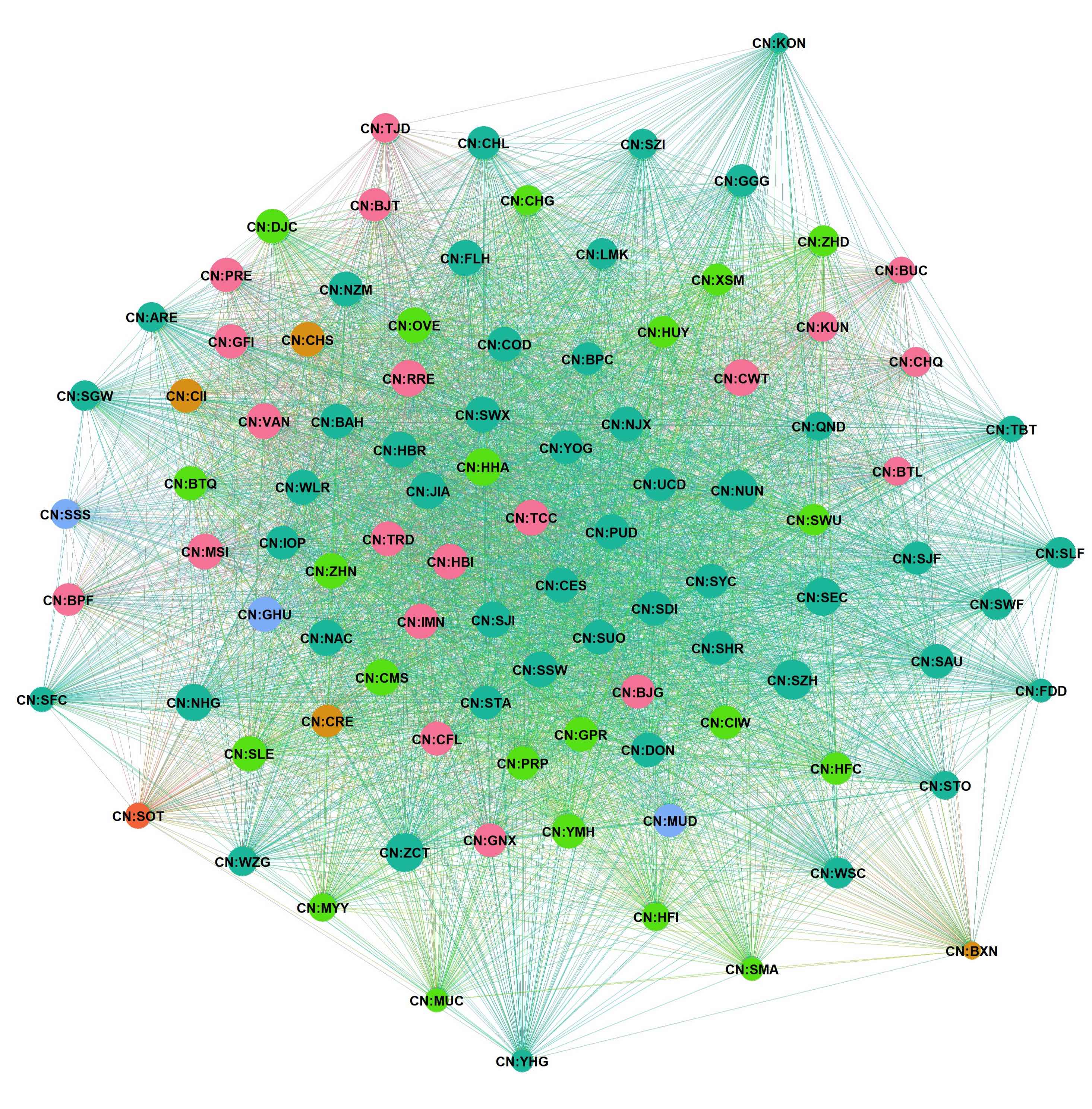

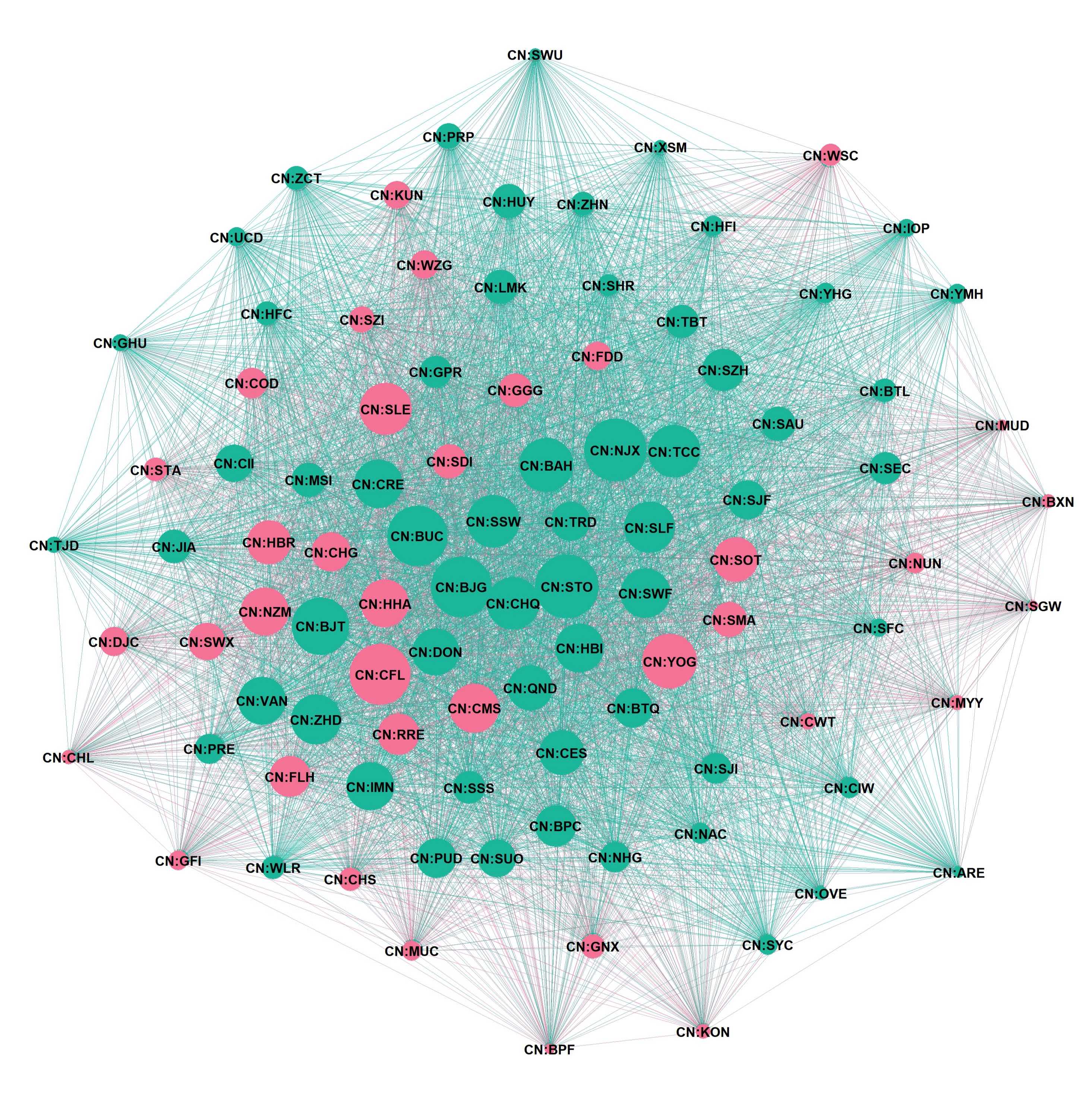

Visualizing Systemic Risk: Decoding Network Structures

Network analysis is employed to model systemic risk by representing financial institutions as nodes and their interdependencies as directed edges. The strength of these connections is quantified using Diebold-Yilmaz spillover indices, which measure the extent to which shocks to one institution propagate to others. These indices are calculated based on the variance decomposition of forecast error, effectively tracing the directional flow of risk between developers. Specifically, the methodology assesses how much of the forecast error variance of one developer can be attributed to shocks originating from others, thus establishing a weighted, directed network representing systemic interconnectedness. This allows for the identification of systemically important institutions and potential contagion pathways within the financial system.

The ForceAtlas2 algorithm is a force-directed graph layout specifically designed for visualizing large networks. It operates by modeling nodes as repelling particles and edges as spring-like attractors, iteratively adjusting node positions to minimize overall energy and achieve a balanced layout. In the context of systemic risk analysis, this results in a visual representation where highly interconnected firms cluster together, indicating strong directional relationships. These clusters, and the nodes with a disproportionately high number of connections (high degree centrality), are readily identifiable as potential systemic risk contributors and points of failure within the financial network, allowing for focused risk assessment and mitigation strategies. The algorithm’s emphasis on minimizing edge crossing further enhances readability and clarifies the network’s underlying structure.

Initial network analyses of financial institutions revealed significant spillover effects correlated with regional concentrations; a shock to one firm within a geographic area demonstrably increased the probability of distress for its regional peers. However, subsequent analyses conducted over time indicated a decline in the strength of these regional connections. Investor attention increasingly focused on idiosyncratic risk factors – the specific vulnerabilities of individual firms, such as capital structure, asset quality, and management practices – rather than broad regional exposures. This shift is evidenced by a weakening of directional connectedness between firms located in the same region, and a corresponding increase in the importance of direct, firm-to-firm linkages based on interbank lending and shared exposures.

Heterogeneous Risk: Distinguishing Patterns of Vulnerability

Research indicates that privately-owned enterprises in the Chinese real estate sector demonstrate a heightened sensitivity to adverse market events when contrasted with their state-owned counterparts. This increased vulnerability stems from greater reliance on external financing and a comparatively limited access to implicit government support, amplifying the impact of economic downturns or policy shifts. Consequently, private developers are more prone to experiencing liquidity crises and defaults during periods of market stress, creating a cascading effect – or contagion – that can rapidly spread through the wider financial system. This dynamic suggests that shocks affecting private enterprises are not isolated incidents, but rather potential catalysts for systemic risk, demanding focused monitoring and proactive intervention strategies.

The contrasting behaviors of State-Owned Enterprises and privately-owned developers necessitate differentiated policy approaches to stabilize China’s real estate sector. Research indicates that private developers demonstrate heightened sensitivity to market downturns, making them more vulnerable to contagion effects, while SOEs exhibit greater resilience. Consequently, interventions designed to mitigate risk cannot be universally applied; instead, they require dynamic adjustment based on evolving risk perceptions within each ownership type. Policymakers must recognize that the relative vulnerability of SOEs and private enterprises isn’t static; it fluctuates over time, influenced by macroeconomic conditions and specific market events. Effective strategies therefore demand ongoing monitoring and the capacity to tailor support mechanisms, such as credit access or regulatory oversight, to address the unique challenges faced by each sector and prevent systemic instability.

A granular comprehension of differing risk profiles within China’s real estate sector is paramount for constructing robust strategies against systemic financial risk. The sector doesn’t present a uniform level of vulnerability; privately-owned enterprises demonstrate a heightened sensitivity to market fluctuations compared to their state-owned counterparts. Consequently, broad-stroke policy interventions risk being ineffective, or even exacerbating instability. Instead, targeted approaches, dynamically adjusted to reflect evolving risk perceptions within each ownership type, are essential. By acknowledging these nuanced vulnerabilities and tailoring mitigation efforts accordingly, policymakers can proactively address potential contagion effects and bolster the overall resilience of the Chinese real estate market, preventing wider economic repercussions.

The study meticulously charts the interconnectedness of Chinese real estate firms, demonstrating how shocks propagate through the network. This resonates with Immanuel Kant’s assertion: “Begin from the conditioned and work back to the condition.” The research doesn’t simply observe the crisis; it systematically decomposes the variance of volatility, tracing spillover effects back to their sources within the network. By examining the conditional dependencies – how one firm’s volatility is conditioned on others’ – the analysis illuminates the underlying structure driving the real estate crisis and offers a framework for understanding systemic risk. This approach aligns with a Kantian method of discerning causal relationships through careful observation and logical deduction, revealing the conditions that give rise to observed phenomena.

Where Do We Go From Here?

The application of network analysis to Chinese real estate volatility reveals a landscape of interconnectedness-a predictable outcome, perhaps, given the sector’s inherent systemic risk. However, the persistence of state ownership as a differentiating factor demands further scrutiny. While connectedness metrics quantify spillover, they do not inherently explain the why of transmission. Is observed variance decomposition merely a consequence of market mechanics, or are deliberate interventions-subtle or overt-shaping the flow of risk? The current framework identifies patterns of influence, but struggles to disentangle correlation from causation.

Future work must move beyond descriptive connectedness and embrace dynamic modeling. A static network, however elegantly constructed, offers limited insight into evolving crisis dynamics. Integrating behavioral factors-investor sentiment, herding behavior, and information cascades-promises a more nuanced understanding of spillover mechanisms. Furthermore, extending the analysis to incorporate financial institutions and international markets is crucial, given the sector’s global implications.

The present study illuminates the what of volatility transmission, but the fundamental drivers remain elusive. If a pattern cannot be reproduced or explained, it doesn’t exist. The challenge lies not simply in mapping the network, but in deciphering the underlying logic that governs its behavior.

Original article: https://arxiv.org/pdf/2602.19740.pdf

Contact the author: https://www.linkedin.com/in/avetisyan/

See also:

- United Airlines can now kick passengers off flights and ban them for not using headphones

- Crimson Desert: Disconnected Truth Puzzle Guide

- All 9 Coalition Heroes In Invincible Season 4 & Their Powers

- Mewgenics vinyl limited editions now available to pre-order

- Grey’s Anatomy Season 23 Confirmed for 2026-2027 Broadcast Season

- Assassin’s Creed Shadows will get upgraded PSSR support on PS5 Pro with Title Update 1.1.9 launching April 7

- Viral Letterboxd keychain lets cinephiles show off their favorite movies on the go

- The Original Resident Evil is Finally Available on Steam

- Crimson Desert Guide – How to Pay Fines, Bounties & Debt

- Does Mark survive Invincible vs Conquest 2? Comics reveal fate after S4E5

2026-02-25 00:16