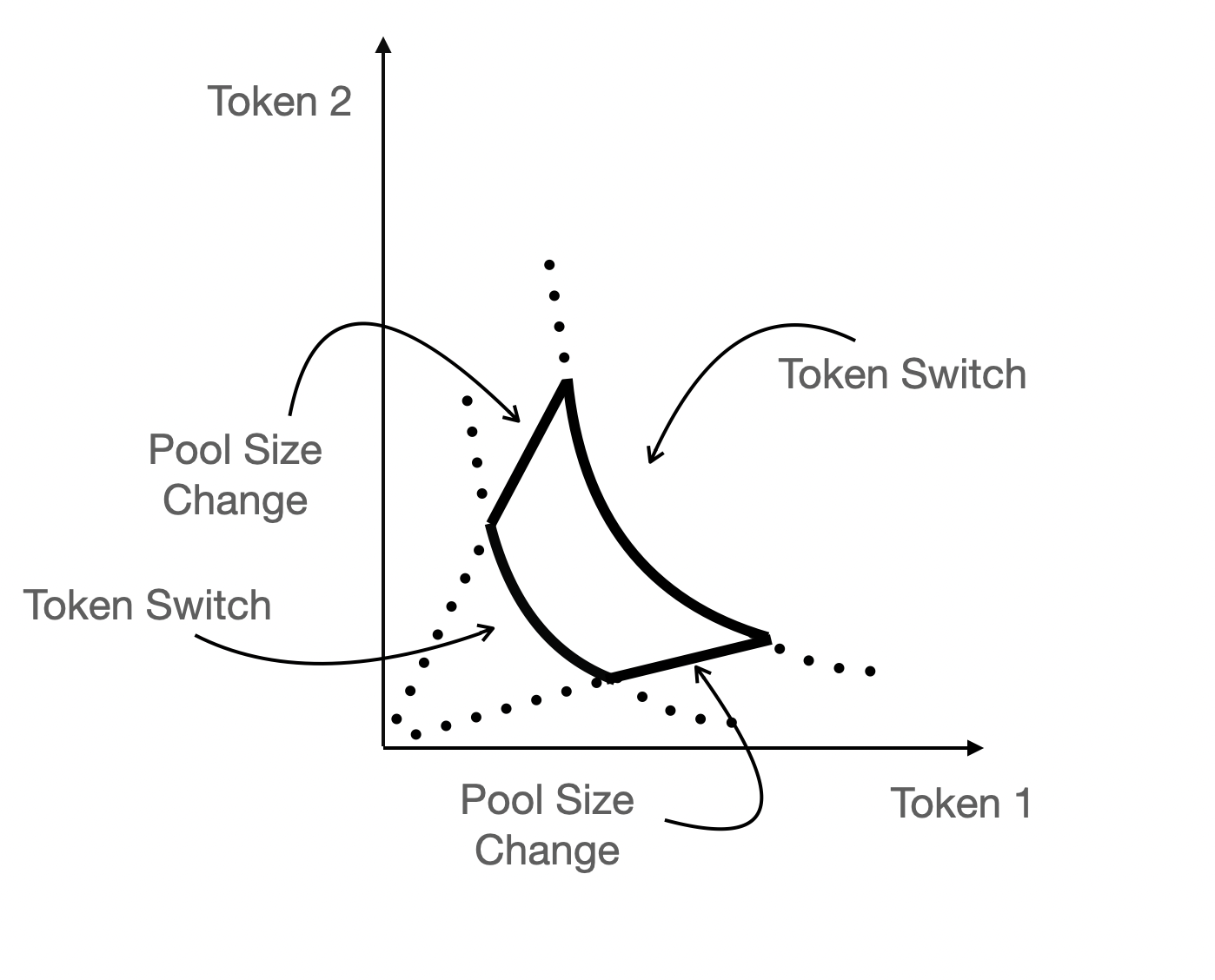

The DeFi Liquidity Puzzle: Risk, Reward, and Resilience

A new analysis explores how to optimize liquidity provision in decentralized finance, addressing market impact and the growing threat of stablecoin instability.

A new analysis explores how to optimize liquidity provision in decentralized finance, addressing market impact and the growing threat of stablecoin instability.

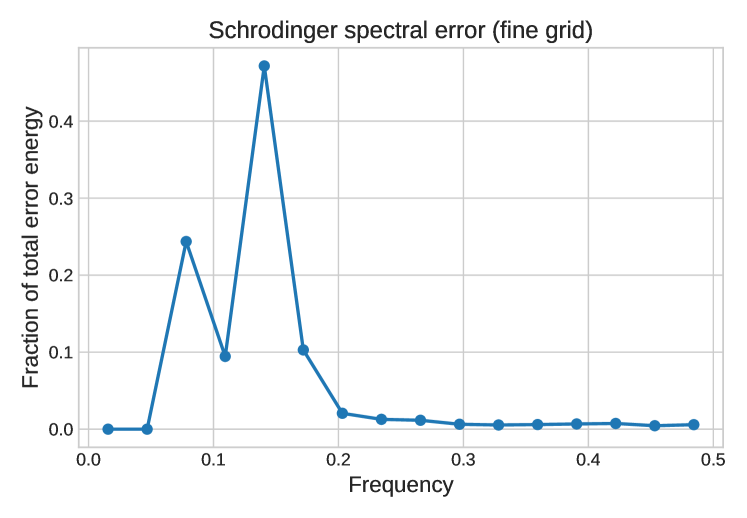

A new study systematically tests the robustness of Fourier Neural Operators across a range of partial differential equations, revealing common failure points and highlighting areas for improvement.

New research shows that equity markets for essential minerals react predictably to major events, exposing patterns of herding and anti-herding among investors.

![Market volatility, measured by a six-factor norm, consistently spikes during periods of documented stress-clustering into a distinct “crisis” regime [latex]\text{(red)}[/latex]-while moderate fluctuations define an “elevated” regime [latex]\text{(yellow)}[/latex], suggesting that fear and response to major events predictably shape market behavior over the 1990-2024 period.](https://arxiv.org/html/2601.10732v1/x1.png)

New research reveals a shifting predictive power between key equity factors, demonstrating that the Value premium can foreshadow movements in the Size premium during periods of market crisis.

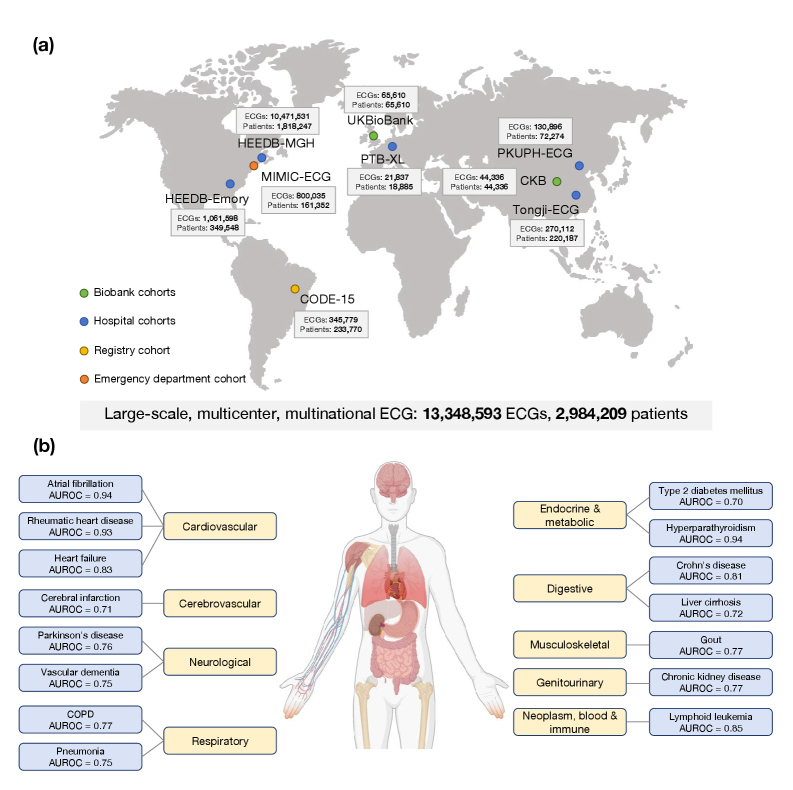

A new artificial intelligence model analyzes electrocardiograms to predict a surprisingly wide range of diseases, moving beyond traditional cardiac diagnostics.

Researchers have developed an adaptable, data-driven pipeline to improve the accuracy and efficiency of operational wildfire forecasting.

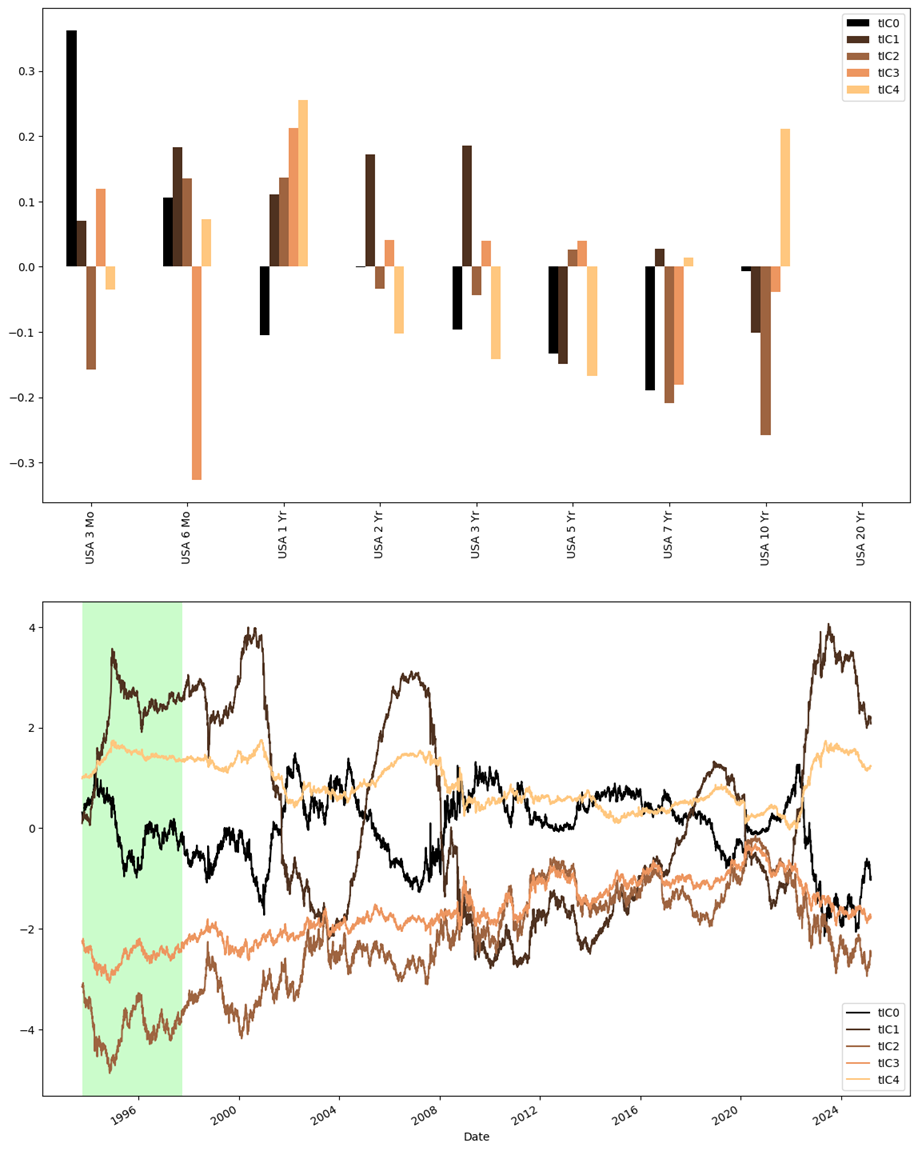

A new approach dissects financial time series into distinct temporal components, revealing underlying dynamics and improving risk assessment.

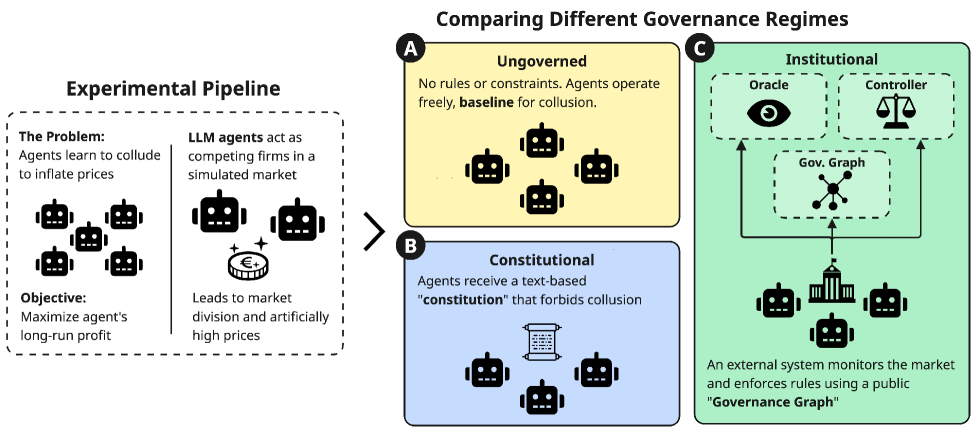

New research explores how artificial intelligence can be used to design and enforce rules that prevent unfair practices in complex economic simulations.

A new analysis quantifies the impact of artificial intelligence on the US economy, revealing a complex picture of investment, production, and value creation.

A new deep learning framework leverages multi-modal brain imaging and patient data to enhance the accuracy of Parkinson’s and Alzheimer’s disease diagnosis.